Alumina giant Alcoa pulled out of its JV with FYI Resources - What now?

Published 24-FEB-2023 14:08 P.M.

|

12 minute read

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,097,000 FYI shares at the time of publishing this article. The Company has been engaged by FYI to share our commentary on the progress of our Investment in FYI over time.

With every cloud there’s a silver lining.

On Wednesday, FYI Resources (ASX: FYI) announced that its Joint Development partner Alcoa of Australia had elected to withdraw from its advanced High Purity Alumina (HPA) project.

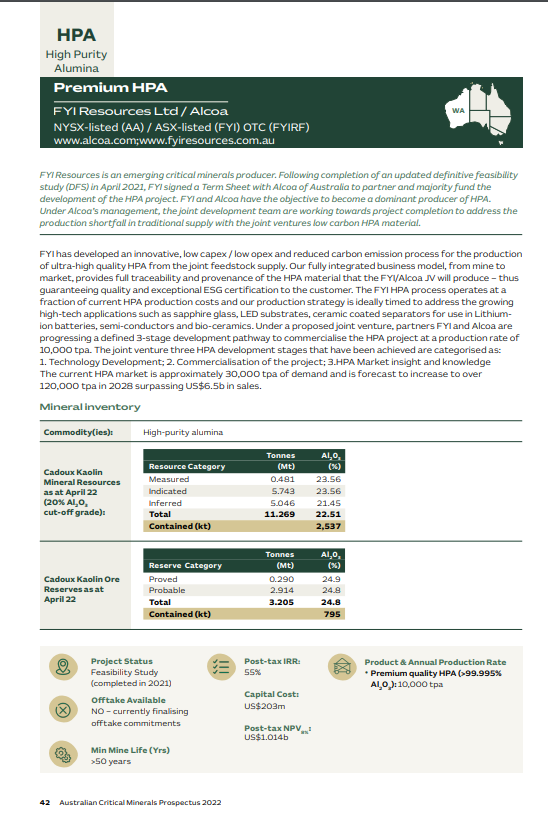

High Purity Alumina is a high tech product increasingly used in batteries, and it's also a key part of LEDs and sapphire glass screens (you may be reading this on your tablet or smartphone with such a screen).

FYI’s project economics remain strong, with its Definitive Feasibility Study indicating US$1.1BN NPV (net present value) on the back of a 10ktpa operation generating an average of US$186M earnings per annum over its 25 year life of operations - this would require capital investment of US$202M .

Alcoa previously was to earn a 65% stake in the project in return for funding 97% of the US$250M project financing expenses.

Whilst the plan for FYI was that Alcoa would take care of the funding and share in the profits, this is no longer going to be the case.

FYI is now back to 100% ownership, in control of its own destiny - albeit without a funding partner locked in.

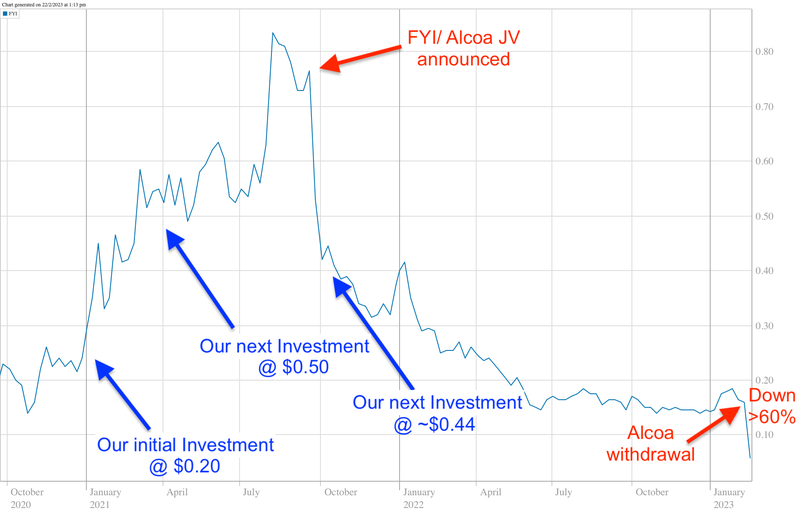

The market reacted to this news negatively, sending FYI shares down over 60% to under 6c, before rebounding yesterday to close at 7.6c.

After reaching the dizzying pre-Alcoa deal heights of over 75c in September 2021, FYI is now trading back at levels last seen mid-2020, despite the substantial progress since.

So now FYI has a current market cap of circa $27M and holds $10.1M in cash, with 100% ownership of the project.

As Investors, we are optimists, and while the market clearly didn’t like the news on Wednesday, there are some positives for FYI.

FYI is in total control now with 100% ownership of the project, and given its not beholden to a much bigger company with different strategic priorities, we think we might start to see FYI accelerate progress.

Alcoa is a large US based multinational aluminium company capped at US$8BN, and while they certainly can bring in financial muscle, industry expertise and networks to the partnership, it is a less agile corporation - in hindsight, they might not have been the best fit to help fast-track an intricate high-tech project like FYI’s.

We think that the story is that a stressed out large corporation which has a core high volume/low margin business under pressure decided to pull the plug on a low volume/ high margin future facing investment.

So the band-aid is well and truly off now, where does that leave FYI?

A lot comes down to potential partnerships and funding arrangements FYI can now pursue in either the private or public sector.

With funding for FYI’s project now substantially more uncertain, the company will need to work overtime to find another pathway.

We are still holding on to our FYI position and we still believe in the technology and project despite the funding uncertainty.

FYI is advancing a project that could transform the high purity alumina (HPA) industry by delivering a cleaner and cheaper product.

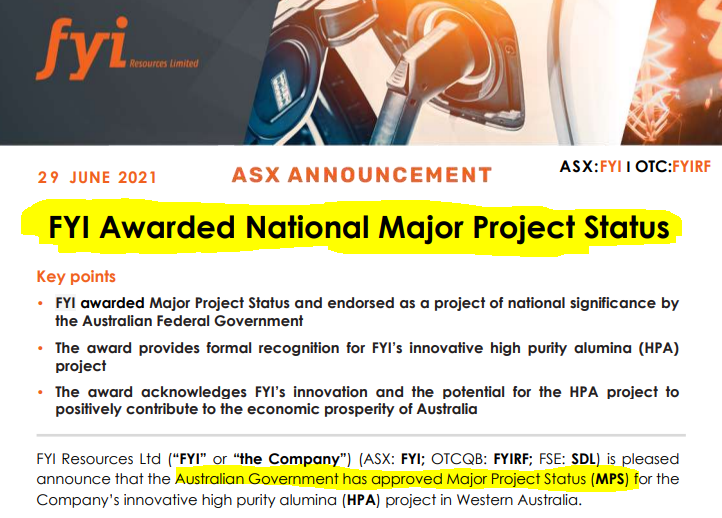

The HPA project has strong government backing, with the Australian Government awarding it ‘Major Project Status' and the WA Government following suit with ‘Lead Agency’ status - meaning that FYI can access government support, both bureaucratic and financial, to fast-track development.

Again, with a US$1.1BN NPV, this is no small project - and could become a nationally significant part of Australia’s battery materials push.

So we expect new partners should start to come forward now that Alcoa has effectively left the building.

With FYI unshackled, our Investment Plan is to hold the majority of our position and see what a more nimble FYI can achieve.

The market for HPA is growing rapidly, largely due to burgeoning demand for lithium ion batteries (in which HPA is a preferred separator component) as well as LED lights.

We remain confident that HPA will play an important role in the battery materials market and FYI is the right exposure for us to this macro theme.

Following Alcoa’s withdrawal news, our ‘Big Bet’ for FYI remains, which is as follows:

Our FYI Big Bet:

“We want to see FYI significantly re-rate by moving into High Purity Alumina (HPA) production and scaling its technology to other HPA projects”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our FYI Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

So what happened?

In September 2021, FYI partnered with the Australian subsidiary of the leading global aluminium producer, Alcoa, to develop its HPA project via a Joint Venture arrangement - essentially both parties would work together in a Joint Development partnership which would be formalised as a JV down the road.

The partners have ever since advanced the project together, with Alcoa chipping in US$5M through the pilot plant stage and towards the doorstep of the Financial Investment Decision (FID) for a demonstration plant.

However, earlier this week Alcoa elected to withdraw from the project.

No reasons were provided in either FYI’s or Alcoa’s announcements on the withdrawal, with both parties remaining cordial.

In our FYI Investment Memo, we highlighted the Alcoa funding as a key risk for FYI:

FYI shares were down over 60% following the withdrawal announcement on Wednesday, but in an encouraging sign, clawed back over 25% yesterday to close at 7.6c.

As investors in FYI, with an Average Entry Price of ~40 cents, this one stings.

However, FYI is a small portion of our Total Portfolio - and it's an excellent reminder to us of the risks involved in investing in development stage small cap stocks.

Whilst the crash was significant, this market response was not unexpected for multiple reasons:

1.) The market is speculating on whether or not FYI’s tech stacks up - with a partner like Alcoa walking away from the project, this is the natural assumption in markets.

Our view is that oftentimes the market overreacts to news like this without trying to first process the impact. It can become more often a “sell first, ask questions later” type day - as emphasised by the 27% clawback yesterday.

We have been Investing in small cap stocks for decades and have seen multiple larger capped partners walk away from smaller partners before.

Typically, these types of deals fall through because larger capped partners need to allocate capital into the efficiency of cash generating business units over more blue sky opportunities.

For the smaller company, this presents opportunities, especially in terms of being more agile with development - whereas for the larger capped company, it just means they will need to pay more when the technology is more advanced and de-risked (which they often don't mind doing).

2.) The market is nervous about the remaining funding required for the project - The demo plant was slated to have a CAPEX of ~$50M and the full scale plant was going to require a further $200M in CAPEX funding.

Under the joint venture agreement, Alcoa was supposed to fund ~97% of this.

The obvious question now is who funds the project from here on out?

This adds a new layer of risk to FYI that shareholders “priced in” to be mitigated through the Alcoa partnership.

With the partnership over, FYI will need to find a new pathway to funding its project.

Given FYI now has a market cap under $30M, and cash on hand of $10.1M as of the end of January, project financing is much more challenging.

That said, FYI’s relatively small Enterprise Value (under $10M ~$20M) may appear as good value for 100% ownership of an advanced HPA project for new investors or existing shareholders looking to average down.

Over the coming period, if FYI can prove a customer base exists for initial production volumes, we would like to think someone should be able to finance the upfront capital costs, and this could be a mixture of debt and equity, or any myriad of other financing options.

We have seen a similar negative market response to FYI previously since we first Invested.

Upon announcing the JV arrangement with Alcoa on 1 October 2021, FYI shares shed over 50% within the space of a month - we suspected at the time that investors were not impressed with FYI giving up so much equity in its project.

Well now FYI has that equity control back, and FYI remains committed to advancing its HPA project.

The question now remains... where does this leave FYI, and what does the company do going forward?

Critical minerals projects attract funding

While the news earlier this week wasn't exactly what we wanted to see, the macro tailwinds for HPA has only strengthened over the last 12 months.

In March 2022, the Australian government added HPA to its updated critical minerals list as part of its 2022 Critical Minerals strategy.

Interestingly, it is also on the US and EU critical minerals lists:

At the same time the Australian government also awarded a $45M government grant for ASX listed Alpha HPA’s High Purity Alumina project in QLD from its $1.3BN Modern Manufacturing Initiative - a part of the nation’s Resources Technology and Critical Minerals Processing Roadmap.

Here's why all of this matters for FYI:

1) FYI’s project has “Major Project Status” from the Federal Government - Major Project Status means the Australian government recognises FYI’s project as significant for the Australian economy and provides additional support.

2) FYI’s project has “Lead Agency” status from the WA government - Lead Agency status also helps at the state government level with project approvals.

3) FYI’s project is listed on Australia's critical minerals prospectus - This is a document that features the biggest, most advanced critical minerals projects in Australia so as to encourage foreign investment into the projects.

We think that all three of these reasons will be helpful for FYI to bring a new partner onboard for its HPA project.

Our view is that FYI’s project could have been passed on by other potential partners primarily because Alcoa had already committed to a partnership with FYI.

Now that Alcoa is gone, FYI may be able to pursue such opportunities that come about from the pathways above.

With that said, below are the several funding options we see for FYI’s project:

Potential funding options for FYI

Government Support

There are a slew of government grants and funding facilities available to FYI, especially given the ESG-friendly and Critical Minerals focus of FYI’s project.

The federal government has been active with its Export Finance Australia (EFA) and the Northern Australian Infrastructure Facility (NAIF) funds.

A recent example, in November the Australian Government committed up to $250M in support for Pilbara Minerals’ Pilgangoora Lithium Operations in WA.

Debt Financing

With a Definitive Feasibility Study (DFS) in hand, debt financing becomes another avenue FYI can pursue for project financing.

FYI’s project economics are relatively strong with a NPV of US$1.1BN and a capital payback period of 3.2 years - this we think is strong enough to make the project attractive for debt financiers.

If FYI can lock in any offtake agreements then debt financing becomes more likely. The key benefit of debt financing is that it is non-dilutive to current shareholders.

New partner

Now that FYI controls 100% of its project it may be able to attract another partner that is willing to provide financing support.

Equity financing

Capital raising via issuing equity is another possibility, although we think at its current market cap and current stage this would be unlikely in the near term.

FYI will want to deliver on a number of milestones and drive a positive re-rating prior to an equity raising for even partial project financing.

The good news is that FYI has substantial cash backing at the moment, above $10M as of 30 January 2023 - especially for its current market cap, giving time for the company to progress its project.

We will have to wait to see how FYI looks to develop its HPA project - the company has stated that it will “revise and redefine the HPA project development with a “speed to market” approach” as a short term priority, which we take to mean that a new plan will hopefully be announced soon.

In either case, we are still supportive of FYI and the HPA project, and are keen to see - and provide our commentary on - what FYI’s forward plan looks like.

Investment Memo Retro and What is next for FYI:

After the announcement earlier this week we decided to do an objective retro on our FYI Investment Memo.

A large part of our memo was dependent on Alcoa’s commitment and so we feel it is redundant now.

To see how FYI performed against our FYI Investment Memo #1 check out the following link:

We now await details of FYI’s new ‘speed to market’ plan for developing the HPA Project.

Once FYI puts forward a detailed plan we will launch our second FYI Investment Memo so be on the lookout for this over the coming weeks/months.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.