FYI to partner with leading Aussie rare earths company in NT

Published 10-MAY-2023 11:00 A.M.

|

15 minute read

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,097,000 FYI shares at the time of publishing this article. The Company has been engaged by FYI to share our commentary on the progress of our Investment in FYI over time.

A new project that could become a globally significant source of rare earths supply.

AND a potential partnership with $867M Arafura Resources - the developer of Australia's only heavy rare earths separation plant.

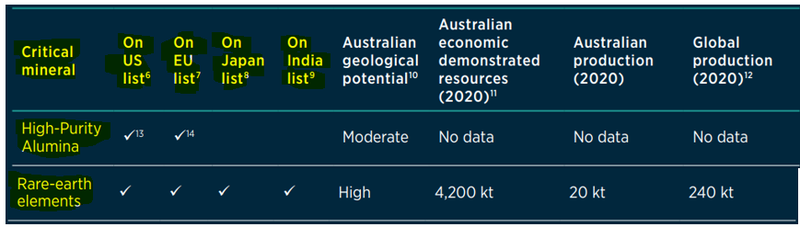

Our critical minerals Investment FYI Resources (ASX: FYI) now has exposure to two sets of critical minerals:

1) High Purity Alumina (HPA)

FYI has a DFS stage project for High Purity Alumina that could be a key pillar of an emerging Australian battery materials industry.

A low volume, high margin business with an NPV (net present value) of US$1.1BN NPV.

This is on the back of a 10ktpa operation generating an average of US$186M earnings per annum over its 25 year life of operations from a US$202M CAPEX.

2) NEW Acquisition Rare earths

FYI is looking to develop a rare earths processing plant.

FYI is aiming to deliver a feasibility study by early 2024, which will be jointly funded by Arafura Rare Earths.

This could dramatically increase Australia’s total rare earths production in a market that is projected to experience 1,000% demand growth through to 2035.

Both HPA and rare earths are highly leveraged to the energy transition and both are listed in Australia’s critical minerals strategy:

Today we will unpack FYI’s entrance into the rare earths sector in Australia, and release our latest Investment Memo on the company.

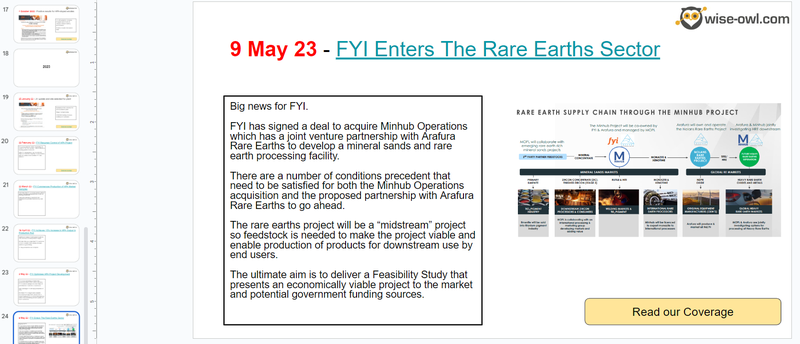

Yesterday, FYI signed a binding heads of agreement to acquire 100% of “Minhub”.

FYI managing director hosted a webinar to talk through the transaction, which can be viewed anytime by registering here.

Watch FYI Managing Director Discuss The New Rare Earths Deal

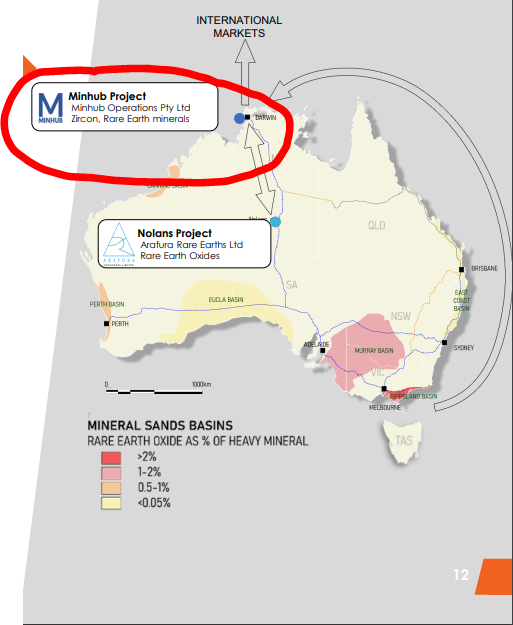

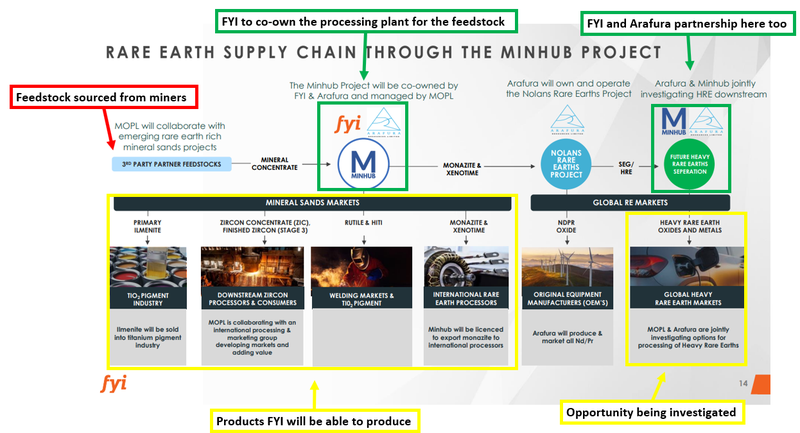

Minhub will ultimately look to develop, construct, and operate a plant in the Northern Territory capable of processing rare earth rich mineral sands deposits.

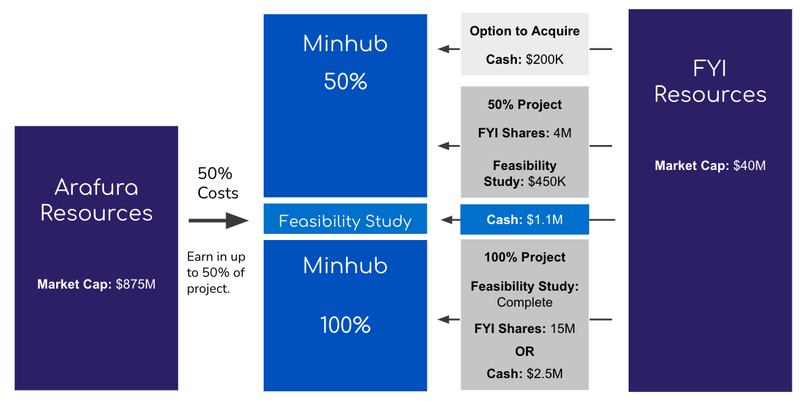

The deal comes with a non-binding co-operation agreement with $867M capped Arafura Rare Earths under which Arafura could end up being FYI’s 50% partner in the Minhub project.

Arafura is building Australia’s only heavy rare earths separation plant and has offtake agreements with Hyundai and Kia as well as MoU’s with GE Renewable Energy.

Arafura also has a history of planning, designing and funding rare earths processing plants with $30M in government funding secured to build a rare earths separation plant as part of the Australian Government’s Modern Manufacturing Initiatives program.

The grant funding available under the scheme is for projects exactly like FYI’s new acquisition.

With the Minhub deal being facilitated by the office of the Northern Territory Major Projects Commissioner, there is a chance FYI’s project could eventually be considered for this type of funding as well.

Arafura have now positioned themselves to take up to 50% of the project as well as first right of refusal to purchase products from the project (xenotime and monazite).

Arafura’s interest in the project is clearly related to the integrated development strategy the company is pursuing at its Nolans rare earths project whereby different ore sources are fed through the company’s processing plant.

The following comment from Arafura’s MD Gavin Lockyer makes this pretty clear:

“Arafura is pleased to explore opportunities associated with the Minhub Project as a possible pathway to expand downstream processing at the Nolans Project”.

For us, Arafura’s interest in the project alone is enough to validate the project’s potential.

On top of this, the existing government support and the prospect of more to come always helps as well.

Below is a summary of what FYI is acquiring and what the project will be able to produce:

You can watch a replay of the presentation by FYI from yesterday: Watch FYI Managing Director Discuss The New Rare Earths Deal

Here is our breakdown of yesterday’s deal

What is FYI acquiring?

FYI is acquiring 100% of “Minhub” - a private company looking to develop a processing plant capable of processing products from heavy rare earth mineral sands projects.

Once the acquisition is complete, FYI would own and operate 50% of the project Arafura own the remaining 50% - the Arafura portion is contingent on a binding agreement being signed between the two companies.

The project will be looking to take rare earths heavy minerals sands feedstock (that was previously considered waste material) and process it into valuable heavy rare earth concentrates.

FYI will then look to sell some of that product into the open markets and some of it to Arafura who can process it further at the Nolan processing plant nearby.

At this stage the project is at the “concept stage” with technical work to commence leading into a pre-feasibility study (PFS) expected to be delivered by early 2024.

In the background the project will be looking to finalise agreements with existing and potential mineral sand producers for product that can be processed once the plant is up and running.

FYI plans to be the project manager through the Feasibility Study, development and operating stages of the project.

Who are the partners?

The major project partner is $867M Arafura Resources.

Arafura is building Australia’s only heavy rare earths separation plant which it has already managed to lock away $30M of grant funding for.

Arafura’s partnership with FYI will be via a co-operation agreement on a 50:50 basis through to a feasibility study being announced.

After the feasibility study Arafura can make a development decision and proceed with the project.

As part of the co-op agreement Arafura also has first rights of refusal on offtakes for two specific products (xenotime and monazite).

On top of all of this FYI and Arafura will also look at a potential partnership on a heavy rare earths downstream plant.

What is FYI paying?

The deal is also conditional on the following being put in place:

- Agreement with Arafura to collaborate and co-fund 50% of the feasibility study.

- An offtake option on heavy mineral concentrates with key suppliers.

- An access agreement with the Darwin port + a binding lease on a site.

- A management contract being agreed with the vendor (this is unlikely to be an issue).

What’s next for FYI’s rare earths project:

- Technical work and offtake discussions with feedstock partners 🔄

- Feasibility Study (due early 2024 - 50:50 funded by Arafura and FYI) 🔄

- Binding agreements between FYI and Arafura (after the feasibility study) 🔲

- Site identification and permitting in Darwin, NT 🔲

FYI now has a two pronged exposure to a wave of capital flowing into the critical minerals space - this forms part of our Big Bet for FYI which is as follows:

Our FYI Big Bet:

HPA is still the main priority, even though the new FYI rare earths project is a great addition to what is now a portfolio of critical minerals development projects.

“We want to see FYI significantly re-rate by moving into High Purity Alumina (HPA) production and scaling its technology to other HPA projects”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our FYI Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

New FYI Investment Memo:

The focus of our previous FYI Investment Memo was the company's High Purity Alumina project.

The acquisition yesterday of a potential company making project is enough to trigger an Investment Memo reset for us.

The acquisition fits in with memo revision condition #2 which we listed in an educational article we wrote in the past.

🎓 To see how we write our Investment Memo’s and what triggers a reset check out the following article: Investment Memo recap and what triggers a reset

Today we launch our NEW FYI Investment Memo, where you can find:

- Why we are Invested in FYI

- The key objectives we want to see FYI achieve over the next 12 months

- The key risks to our Investment thesis

- Our Investment Plan

FYI Investment Memo - LIVE

Date Published: 10-May-2023

Shares Held: 1,097,000

Why we are Invested in FYI

Advanced, DFS stage HPA project for Australia’s battery push

FYI owns 100% of its HPA project. Highlights from the Definitive Feasibility Study include:

- Project NPV: US$1.1BN

- Production: 10kt of HPA per year

- Annual Revenue: US$186M

- Mine Life: 25 years

- CAPEX: US$202M

We think this project is closely aligned with Australian government policy priorities and a push to build out Australia’s battery materials and manufacturing capabilities.

As such we expect that FYI will be able to attract government grants, loans and other financing support to help fund the construction of its HPA small scale production plant which would enable increased product qualification, offtakes and eventually, development of its DFS scale commercial plant.

Additionally, we think that DFS stage critical minerals and battery materials projects should benefit from current market dynamics and FYI’s HPA project is well positioned to benefit from this trend.

Potential for fast-tracked development of a major Australian rare earths project

FYI is looking to develop a rare earths processing plant with a feasibility study due for completion in early 2024.

FYI has proven highly capable of delivering feasibility studies in the past with its HPA project and we think their expertise should help the company deliver the feasibility study on schedule.

Based on estimates of potential volumes processed at the proposed facility, the output of the project could prove equivalent to:

- >3,000tpa of NdPr, which would be ~10% of the market for this rare earths product as of 2020; and

- >350tpa of Dysprosium (Dy) + Terbium (Tb), which would be equivalent to ~20% of the global market.

Critical minerals exposure, favourable market dynamics

The HPA market is expected to move into deficit in 2024.

With the cost of FYI’s HPA output expected to be under half of the current conventional method (that delivers most of the current HPA supply), the opportunity to substantially disrupt this industry remains on the cards.

With regards to its potential rare earths project, FYI’s pending investment and subsequent development of a rare earths processing hub in partnership with Arafura Rare Earths could prove to be a key plank of Australia’s ability to build out its rare earths supply chain.

The rare earths market is forecast to experience 1000% demand growth by 2035.

ESG focussed company, suitable for institutional investment

We back FYI’s ESG-centric approach, with its process set to replace the current and prevalent more expensive, energy intensive and polluting methods.

We think this will appeal to battery manufacturers and automotive companies as key customers, as well as larger institutional investors.

Projects located in Australia

Currently global processing of both rare earths and HPA are dominated by the Chinese market.

The US and Europe are looking to “friendshore” critical minerals, providing generous tax incentives through legislation like the Inflation Reduction Act.

As FYI’s processing facility is located in Australia, it may be eligible for these tax incentives and a more attractive product than if these minerals were produced in China.

What we expect FYI to deliver

Objective #1: Advance HPA project via small scale production plant

In order to advance the HPA project under its now 100% ownership structure, FYI has opted to pursue a small scale production plant which is targeting output of ~1,000 tpa.

The small scale production plant will enable more potential customers to see if FYI's HPA is the right product for them.

As the HPA project becomes further de-risked, and more product qualification takes place using the output of the small scale production plant, potential customers should become increasingly interested in securing output.

We’re looking for FYI to secure at least one offtake for its HPA product over the term of this Investment Memo. We’ll reassess our Investment Memo should FYI achieve all of these milestones.

Milestones

🔄 Select a preferred engineer for small scale production plant

🔲 Secure government grant funding (applications pending)

🔲 Release CAPEX and OPEX figures for small scale production plant (December 2023)

🔲 Complete construction and commissioning of small scale production plant (May 2024)

🔲 Product qualification update

🔲 Enter into first MOU offtake agreement

🔲 Begin financing discussions for commercial plant

Objective #2: Complete Minhub acquisition and deliver rare earths Feasibility Study

FYI has signed a deal to acquire Minhub Operations which has a joint venture partnership with Arafura Rare Earths to develop a mineral sands and rare earth processing facility.

There are a number of conditions precedent that need to be satisfied for both the Minhub Operations acquisition and the proposed partnership with Arafura Rare Earths to go ahead.

The rare earths project will be a “midstream” project so feedstock is needed to make the project viable and enable production of products for downstream use by end users.

The ultimate aim is to deliver a Feasibility Study that presents an economically viable project to the market and potential government funding sources.

Milestones

🔲 Finalise and settle Minhub acquisition

🔲 Technical work and offtake discussions with feedstock partners

🔲 Feedstock offtake(s)

🔲 Complete first part of Minhub Operations acquisition (50%)

🔲 Arafura commits to 50% of Feasibility Study cost

🔲 Site selected in Darwin

🔲 Permitting in Darwin

🔲 Arafura makes development decision (commits to building project)

🔲 Complete second part of Minhub Operations acquisition (move to 100% ownership of Minhub Operations)

🔲 Bonus: rare earths offtake with an OEM (original equipment manufacturer)

What could go wrong?

Ongoing financing risk

As of March 31st 2023, FYI had ~$9M in the bank.

This is enough for near term plans, however as FYI is not yet generating revenue, it does rely on either capital markets, government grants, or other financing facilities to progress with its plans.

Both the HPA small scale production plant and the rare earths project (including the feasibility study) have yet to be determined capital costs.

Should these costs prove to be too expensive for FYI and should financing not be secured for either or both projects, FYI may need to raise capital to progress the development of these projects.

Technology scale up risk

FYI’s process flowsheet and technology has been proven in the lab and on a pilot plant level, but has yet to be tested at scale. Scaling up the process could prove difficult, unachievable or not financially feasible.

Competition / substitution risk

FYI’s technology is new and seeks to replace the current conventional method (hydrolysis of aluminium alkoxide, a process that has not been substantially changed since the 1880s).

However, there could be yet another new technology that emerges that proves superior or more popular, which would be detrimental to FYI’s business.

Project Funding Risk

Building and constructing processing plants can be expensive.

FYI will need to secure a pathway to funding for the HPA small scale plant, HPA large scale production facility and rare earths processing facility.

Macro theme risk

There could be unforeseen changes to the HPA market that could alter demand, impacting the viability of FYI’s project. The same applies to the rare earths market.

Delay risk

There could be delays in development of both projects, impacting newsflow and the FYI share price. Small caps thrive on consistent delivery of projects to a timeline, and conversely, frequently suffer when newsflow dries up and timeframes are stretched.

Market risk

The broader market could suffer due to a range of macroeconomic factors or sentiment changes. This could exacerbate financing risk.

What is our Investment plan?

We first invested in FYI at 20c and then increased our position at 50c and 44.4c.

In line with our standard investment strategy for small cap investments we de-risked around 17% of our FYI Total Holdings in the lead up to the Alcoa JV catalyst.

We still maintain around 83% of our Total Holdings in FYI and intend to hold the majority of this position until the Feasibility Study is completed for the proposed rare earths project OR until the funding for the small scale production facility is secured.

If the share-price runs up in the lead up to either of these Objectives being completed we will sell up to an additional 20% of our Total Holdings.

We’ll re-evaluate our investment plan following the completion of either of these Objectives.

Our FYI Progress Tracker:

Below is the FYI Progress Tracker document.

We will use this internally to keep up to tabs on the company's progress. It shows how the project was brought into FYI and the progress made up to today, along with what we want to see the company achieve next.

Click here to view our FYI Progress Tracker

Our new FYI Investment Memo:

Read our new FYI Investment Memo where you can find:

- Why we Invested in FYI

- Our long term bet - what we think the upside Investment case for FYI is.

- The key objectives we want to see FYI achieve

- The key risks to our Investment thesis

- Our Investment Plan

- A retrospective on our last FYI Investment Memo (click the tab labelled FYI IM-1)

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.