EMN’s North American battery metals push gathers steam

Disclosure: S3 Consortium Pty Ltd (The Company) and Associated Entities own 1,490,000 EMN shares at the time of publishing this article. The Company has been engaged by EMN to share our commentary on the progress of our Investment in EMN over time.

It’s a remarkable turn of events.

Canada now supplies more goods to the US than China.

In less than a year, the $520BN US Inflation Reduction Act has already started altering the fabric of the US economy.

The legislation promises to further nearshore US supply chains away from China and increasingly towards countries deemed friendly to the US, like Canada.

And it’s increasingly clear that Canada will be a key part of the US battery materials supply chain too.

We know Canada is developing a massive battery hub in Quebec. General Motors, Ford, POSCO and others have all set up camp here.

This is also where one of our Investments has a prime piece of real estate, on which it intends to build a battery metals processing plant.

The battery metal is manganese - an essential raw material in most lithium-ion batteries.

And our Investment is Euro Manganese (ASX:EMN).

There is currently no high purity manganese processing capacity in North America.

EMN wants to change this.

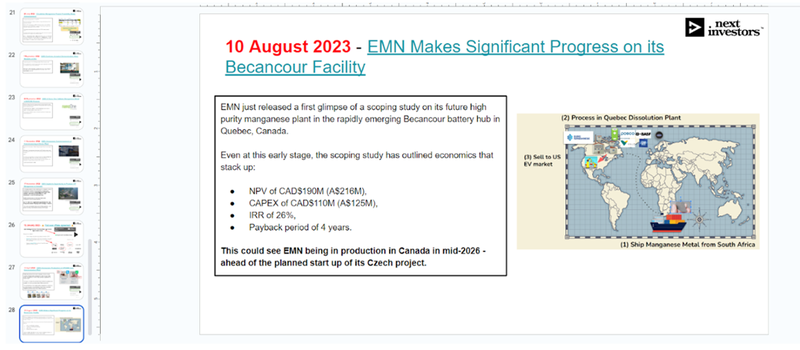

EMN just released a first glimpse of a scoping study on its future high purity manganese plant in the rapidly emerging Becancour battery hub in Quebec, Canada.

Even at this early stage, the scoping study has outlined economics that stack up:

- NPV of CAD$190M (A$216M),

- CAPEX of CAD$110M (A$125M),

- IRR of 26%,

- Payback period of 4 years.

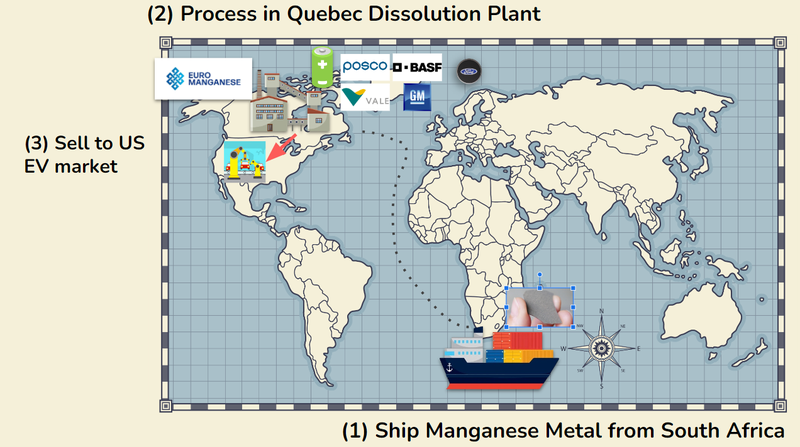

We also learnt that part of EMN’s strategy is to feed its North American processing plant with feedstock from South Africa, having signed an MOU with the largest supplier of high purity manganese metal outside of China.

This could see EMN being in production in Canada in mid-2026 - ahead of the planned start up of its Czech project.

The Canadian plant is part of EMN’s two pronged strategy to ultimately provide BOTH North America and Europe with high purity manganese.

EMN’s Czech project is a tailings rehabilitation project with a DFS that outlines an NPV of US$1.34BN ($2.05BN).

At the Czech Republic project, EMN has already secured an offtake term sheet for its and recently awarded an EPCM contract to help build the European high purity manganese project.

The key catalysts we’re watching for in the Czech Republic are:

- Potential offtake(s) from a large pool of 34 interested parties

- Material updates on the financing of upfront capital costs for the project

Both of which could surprise the market.

So while we wait for more news out of the Czech Republic project, we’re glad EMN has been proactive in cementing its role in the Western EV supply chain as competitive tension builds around its products.

The details from the North American high purity manganese plant are a fascinating glimpse into what could be possible for EMN in Quebec...

Becancour is a small town, but is suddenly brimming with a who’s who of battery supply chain companies.

The town of roughly 13,000 now has these global giants pouring more than $4BN into the area:

- BASF SE, $69BN capped chemical chemical company (world’s largest).

- POSCO - $58BN capped Korean steel giant (now moving quickly on batteries).

- General Motors - US$50BN capped US carmaker.

- Ford - another US$50BN capped carmaker.

- Vale SA - $94BN capped Brazilian mining titan.

All the companies with ingredients needed for batteries (or needing batteries), and EMN could be the missing piece of the puzzle with its high purity manganese.

Currently China accounts for over 90% of the global high purity manganese manganese market.

High purity manganese is necessary for the next generation of EV batteries and there are only a handful of companies in the West that are anywhere close to meeting the wave of demand projected for this battery material.

With that fact in mind, we think EMN has an outsized role to play in the North American battery push.

At a high level - today’s scoping study news shows how EMN can get cashflows quicker, enter the North American market and effectively stamp its authority as the leading Western source of high purity manganese.

Today’s announcement revealed some preliminary numbers for the EMN plant in Quebec.

Here are the key points from today’s announcement:

- Quick 2 year build out delivering cashflows to EMN sooner - EMN is targeting production from the plant in 2026.

- Good economics without including any government help - NPV of CAD$190M ($216M), CAPEX of CAD$110M ($125M), IRR of 26%, payback period of 4 years. All of this shows that even if the US or Canadian governments don’t chip in, the plant can make money.

- Memorandum of Understanding (MoU) with South African manganese metal producer - this MoU enables EMN to supply the plant with material which will use EMN’s technology to produce the products that North America needs for its EVs.

Currently capped at ~$74M, we see EMN as capable of delivering a major re-rate if it can transition into a high purity manganese producer.

There’s precedent for this type of re-rate as well - Lynas Rare Earths achieved a peak market cap of more than $10BN and Syrah Resources also hit a $1.9BN market cap.

By transitioning to becoming producers, Lynas and Syrah effectively were the first large scale non-China sources of rare earths and graphite production - both materials crucial to the energy transition.

Noting that EMN current CEO Matt James is a Lynas alumni, we want to see him do it again, this time with EMN.

Matt James will be providing a conference call update on Tuesday, September 12, 2023 at 4pm AEST - we’ll be listening in:

Click here to register for the EMN conference call

Here’s our EMN Big Bet...

Our EMN Big Bet:

“EMN significantly re-rates to a $1BN+ market cap on becoming a High Purity Manganese producer.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our EMN Investment Memo.

To visualise what EMN has done since we Invested, check out our Progress Tracker:

Why EMN’s North American push matters...

The justifications for EMN’s move into North America are straightforward:

- Massive ramp up in North American high purity manganese demand - demand is projected to more than triple from 250,000 tonnes per year in 2027 and over 800,000 tonnes per year by 2031. EMN’s planned 48,500 tonnes per year plant could provide for ~20% of this demand.

- Need for secure supply chains of critical raw materials - the US wants to wean itself off Chinese supply of critical raw materials like high purity manganese.

- And, the potential to benefit from US government incentives - to achieve this, the US is implementing domestic/friendly content quotas, with tax incentives for batteries that meet these requirements.

EMN is targeting production from the plant in 2026, just in time to catch the start of the wave of high purity manganese demand.

As an added bonus, EMN’s strategic positioning in the Becancour battery hub allows it to literally tap right into other battery projects in the area.

As per details from today’s announcement - there is an opportunity for EMN to actually pump liquid high purity manganese into other battery projects.

This is a new product for EMN, called “high-purity manganese sulphate solution” or HPMSS for short:

“An HPMSS product could be pumped as a solution to nearby precursor cathode active materials ("pCAM") manufacturers, which eliminates the need to crystallize, dry and package an HPMSM product. As HPMSM is ultimately dissolved in water by pCAM plants, delivering a solution saves costs and reduces water consumption and CO2 emissions.”

In order to make this possible, EMN plans to take high purity, selenium free manganese metal from an established South African producer and ship the feedstock to the plant in Quebec where it will be converted into the products needed for batteries.

(Sidebar: selenium is a nasty contaminant that battery manufacturers want to avoid.)

And to make this all possible, EMN signed a MoU with South African high purity manganese metal producer, Manganese Metal Company, who has already provided samples to EMN.

This is how we see it all working:

Why is EMN doing this though?

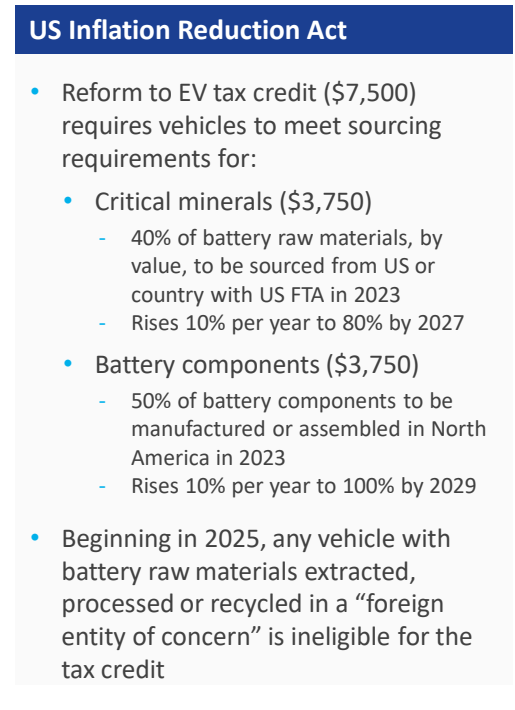

A large part of it comes down to the US Inflation Reduction Act and recent regulatory updates to that, which outline domestic/friendly quotas for battery production.

Below is how these Inflation Reduction Act measures will work:

(Source)

So EMN’s foothold in Quebec would potentially allow EMN to benefit from these requirements, making any offtake from the plant more valuable to nearby battery makers.

All up, it's clear that the world of high purity manganese is rapidly changing and we expect the material to go mainstream in the coming years.

In a sign of where things are going, $17BN capped metals producer South32 is now currently looking at producing 60 ktpa (contained Mn) from its Hermosa asset in the USA.

The mostly zinc/lead mine also contains manganese, and South32 is doing test work to produce high-purity manganese sulphate.

But the demonstration plant is due to be built by South32 in 2025.

EMN already has a demonstration plant working in the Czech Republic, and EMN’s accelerated plan for a full scale North American plant could be up and running by 2026.

There’s a great Fastmarkets interview with South32’s VP of Battery Raw Materials, Alex Volante, explaining the move:

It’s increasingly clear that industry momentum is building for high purity manganese, which was underlined by a recent EMN note we viewed from Canaccord Genuity’s esteemed battery materials analyst Timothy Hoff.

In that update, there was a price target of $1.15 attached to EMN:

While that price target does look interesting, we should be clear that analyst price targets are based on a number of assumptions that may be incorrect - they (or us) don't have a crystal ball.

It’s definitely possible EMN does not reach these share prices. EMN is subject to a number of risks, some of which we list in our Investment Memo. Never invest on a price target alone, and always do your own research.

Going forward, here’s what we expect from EMN as it pursues both the Czech Republic project and its North American plant.

What’s next for EMN?

Here is what we will be watching for from EMN over the next 12 months (drawn from latest presentation):

Delivery of North American Feasibility Study 🔄

Having now completed a scoping study on the Becancour project, EMN has selected WSP Canada Inc to complete a feasibility study on the Canadian battery metals hub opportunity.

So it makes sense that EMN is pursuing opportunities in North America (more specifically Quebec).

The US and EU sealing a battery materials pact would be a boon for EMN’s North American plans as hinted at in this particular article from February which caught our attention:

Czech Republic: Shipment of on spec products to potential customers 🔄

This would mark a big step for EMN, showing the Czech Demonstration Plant is capable of delivering products (particularly the sulphate product) to end users.

These end users would then be able to further test EMN’s products and their suitability for EV batteries among other use cases. This leads into offtakes and financing discussions.

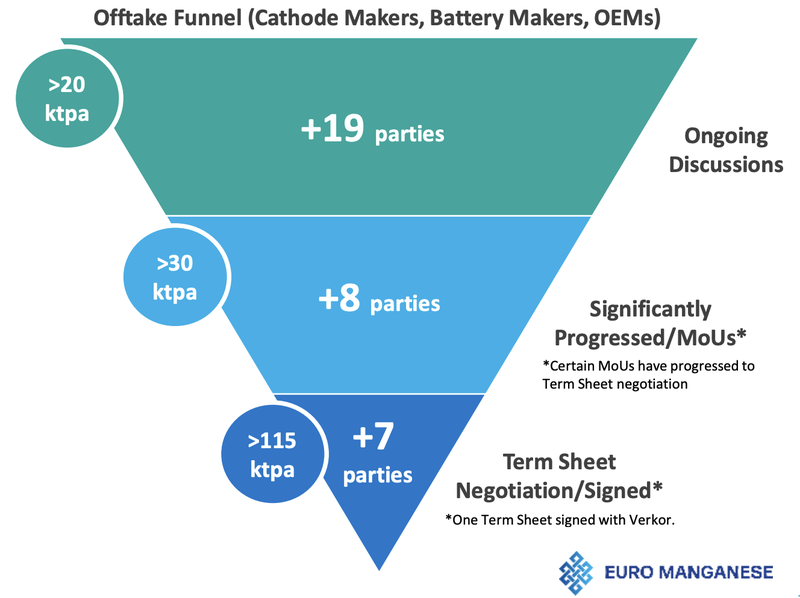

Czech Republic: Progress on offtake front 🔄

EMN signed an offtake term sheet with Verkor in January - hopefully the first of many.

We’re comfortable with EMN maximising value by extending offtake negotiations given demand for over 100% of EMN’s annual production capacity.

While the market may be impatient with EMN’s progress on offtakes, we’re Invested in EMN for the long haul and aware that rushing into offtakes in the current demand environment could detract from the future economics of the EMN’s project.

As we highlighted above, EMN is at the “Term Sheet Negotiation” stage with at least six other parties, so we hope the company can close out these deals soon:

(Source)

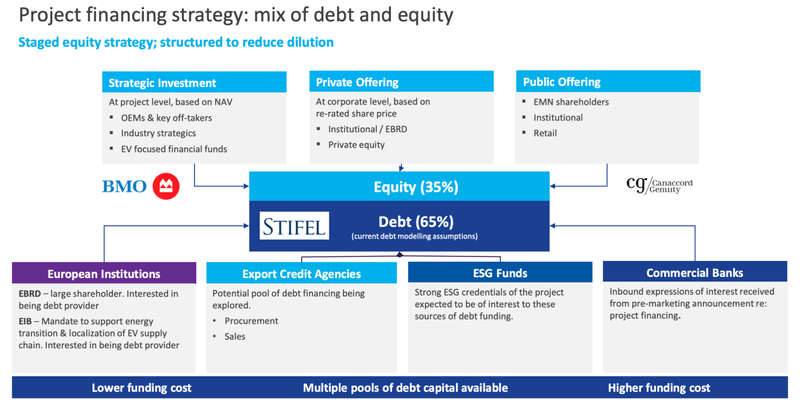

Czech Republic: Progress with project financing and Final Investment Decision (FID) 🔄

To reach a Final Investment Decision (FID), EMN needs to convert offtakes into financing - the two depend on each other.

So to get to a FID, EMN will need to lock in project financing - we expect EMN to lean on:

- Its finance advisor, US financial services company Stifel (market cap ~US$6BN).

- EMN’s existing large shareholder - the European Bank for Reconstruction and Development (EBRD)

- European debt provider - European Investment Bank (EIB) which is mandated to support energy transition projects to help build out a local European battery metals supply chain.

This is the key slide from the latest EMN presentation:

(Source)

We’ve seen major battery makers and EV manufacturers take equity stakes in projects to secure offtakes with other battery materials companies (some in our Portfolio) and we’re hoping a similar thing happens with EMN.

Project level financing would be an ideal scenario, it would demonstrate that EMN’s demand is real and justifies direct investment from an OEM (Original Equipment Manufacturer).

Czech Republic: Permitting 🔄

We’re looking for EMN to secure a “Final Mining Permit” the last bit of the puzzle for EMN to conduct any commercial extraction and processing activities at its Czech Project.

We expect this to be largely a formality given EMN is rehabilitating an old mining deposit and cleaning it up is desirable - but European regulatory bodies can move slowly and this is an important step, especially for financiers.

We note that during the last quarter, EMN hosted a site tour for the Canadian Ambassador to the Czech Republic, and the Canadian Ambassador to the Czech Republic, Ayesha Rekhi, visited the Chvaletice project site in March.

We take these events as evidence of EMN’s stakeholder engagement efforts are working and that the pending permit grant is likely to proceed with the blessing of the relevant Czech authorities.

Risks

Here are the two risks we are most focussed on at this stage for EMN:

There is the possibility that EMN struggles to produce on spec sulphate products from the Demonstration Plant, which would hamper the rest of EMN’s efforts.

Additionally, as EMN is in the financing stage of its project - financing risk could manifest.

This could come in the form of difficulty sealing offtake agreements that lead to potential financiers becoming skittish about funding the project.

EMN will need to finish a feasibility study on its North American plant - and additional CAPEX on top of the Czech Republic project will be required. There is no certainty that EMN will secure financing for either of these projects.

Alternatively if the market sentiment degrades, then projects, no matter how important to securing critical minerals supply, will struggle to get funding as a recession takes hold and the appetite for new investment dries up.

Always remember that small cap investing is risky. Expected AND unexpected things can go wrong, which will negatively impact the share price.

Our EMN Investment Memo

Click here for our EMN Investment Memo which includes:

- Key objectives for EMN

- Why we Invested in EMN

- What the key risks to our Investment thesis for EMN

- Our Investment plan

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.