Growth Portfolio 2018: Resolute Mining Ltd (ASX: RSG)

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

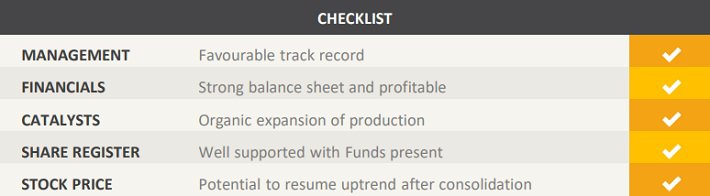

Overview: Resolute Mining Ltd ("Resolute", "the Company") is an Australian gold mining company with operations in Australia and Africa. The Company’s primary focus is on three assets across West Africa and Queensland. The Syama Gold Mine in Mali and the Ravenswood Gold Mine in Queensland are operational, producing approximately 300k oz of gold per annum. The company also owns the Bibiani Gold Project in Ghana. Resolute’s assets have total reserves of 5.3 Moz of gold. We initiated coverage with a ‘buy’ recommendation on 18 February 2016 at $0.46 and our last advice was to ‘hold’ in June 2016 at $1.16.

Catalysts: Syama and Ravenswood are on track to produce ~300koz of gold at sustaining costs of less than US$1,000/oz and have the potential to generate ongoing free cash flow throughout the mine life of 12 years+. Resolute has a strong balance sheet with a cash net of debt of $150 million and little gearing. The updated feasibility study for Bibiani, due in the March quarter, is designed to confirm the commercial viability of the project and enable the development decision after a 40% resource upgrade in October 2017.

Hurdles: Whilst Resolute has a track record of successful mine operations, there is no guarantee it can execute the underground mine plan at Syama or operate Bibiani more efficiently than the previous owner. With a strong focus on West Africa, the Company is subject to geopolitical risks. Global gold prices are volatile and any cyclical decline may negatively impact Resolute’s financial performance and commercial viability of its assets.

Investment View: Resolute offers profitable exposure to the gold mining industry through a portfolio of assets in Australia and Africa. We are attracted to the Company’s production profile and balance sheet and delivery of the updated feasibility study is expected to re-risk the Bibiani project. Exploration and geopolitical risks, as well as the volatile gold price, are principal hurdles. The short-term performance was negatively impacted by increased expenditure, but we remain attracted to the magnitude of the Company’s assets and ability to expand its low-cost production to the benefit of shareholders. We resume coverage and reiterate our ‘buy’ recommendation at $1.22 following a period of share price consolidation.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.