EV1 Key Engineering Appointment - Following the Syrah Playbook

Disclosure: The authors of this article and owners of Wise-Owl, S3 Consortium Pty Ltd, and Associated Entities, own 3,125,000 EV1 shares at the time of publication. S3 Consortium Pty Ltd has been engaged by EV1 to share our commentary and opinion on the progress of our Investment in EV1 over time.

The global decarbonisation push is causing billions of dollars to flow into a rapidly expanding battery industry.

But this push will come to a grinding halt without the raw inputs to the manufacturing process..

One of these critical minerals is graphite – a raw material in all lithium-ion batteries – comprising over 50% of every lithium-ion battery (and over 95% of every battery anode).

With the expected supply shortages, the world’s biggest economies, including the US, EU, India, Japan and Australia have labelled graphite a "critical mineral".

Our 2021 Wise Owl Pick Of The Year, Evolution Energy Minerals (ASX:EV1), just took another step towards developing its shovel ready, graphite development project in Tanzania.

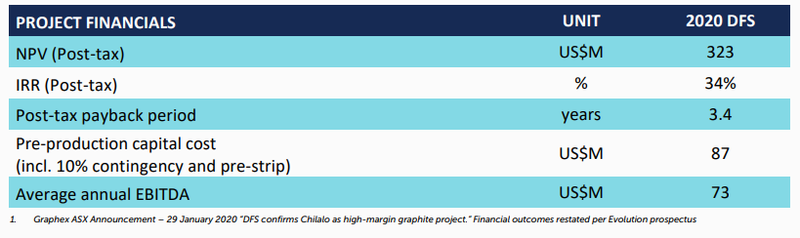

A Definitive Feasibility Study (DFS) has already been completed on the project, showing an NPV of US$323M with a low CAPEX requirement of US$87M, and we think EV1 can get its project into construction at a time when supply is needed the most.

Yesterday , EV1 progressed the development of its project by appointing a "front end engineering and design" (FEED) contractor.

The FEED contractor will ultimately be responsible for designing the processing plant and non-processing infrastructure for EV1’s project, whilst looking at ways to improve plant design and optimise and update estimated capital expenditure.

Interestingly enough, EV1 has appointed the same FEED contractor (CPC Engineering) that delivered ASX-listed Syrah Resources’ Balama project in Mozambique.

Syrah’s plant is the largest integrated natural graphite mine and processing plant globally (measured by annual flake concentrate production capacity).

Syrah is currently capped at $756M, having been valued as high as ~$1.2BN, and has a graphite offtake deal with Tesla.

Importantly, EV1’s executive director Michael Bourguignon was the project manager for the construction of Syrah‘s Mozambique graphite project and has first hand experience working with CPC.

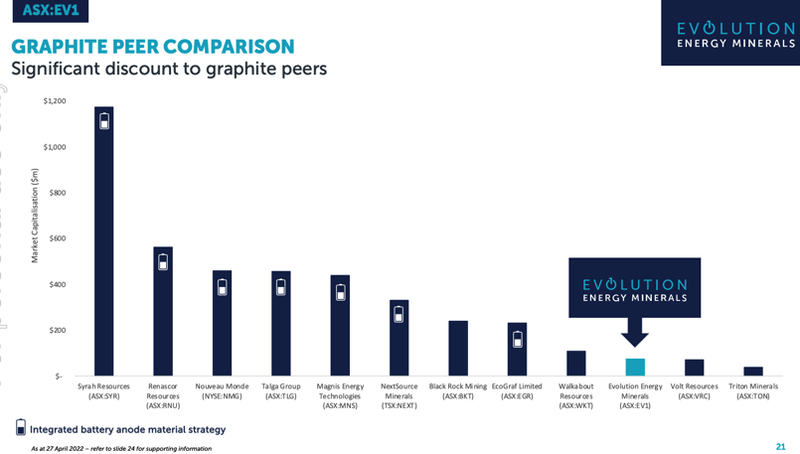

So that’s another similarity between EV1 and Syrah... we can only hope EV1’s market cap starts to catch up to Syrah’s soon.

That's Syrah’s market cap on the left and EV1’s pointed out on the right:

EV1 now has all of the right people needed to try replicate Syrah’s success by bringing its project into production to supply what we think will be a graphite hungry market in the coming years.

With both the FEED works and DFS optimisation work expected to be completed in September 2022, EV1 is positioning itself to have up to date CAPEX estimates for its project before the end of the year — clearing the way for a final investment decision in 2022.

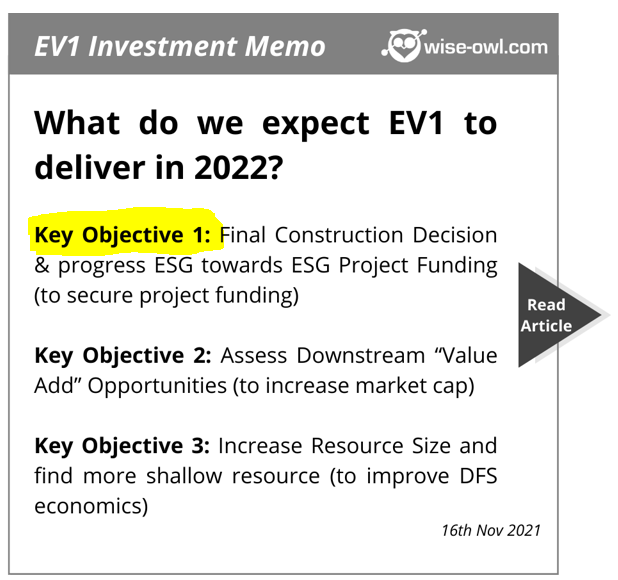

EV1 is now systematically progressing through all of the key objectives that we had set in our 2022 Investment Memo.

With yesterday’s news EV1 has ticked off another key milestone, which is part of key objective #1 - Final Construction Decision & progress towards Project Funding:

More on the announcement

Bringing on the same contractor (CPC Engineering) that handled the design and delivery of $756M capped Syrah Resources’ Balama graphite project in Mozambique is a key part of yesterday’s announcement.

Syrah’s project has the largest integrated natural graphite mine and processing plant globally (measured by annual flake concentrate production capacity) and CPC has a history delivering project design and construction on time and within budget.

So with this appointment, EV1 has brought onboard a team of consultants that have "been there and done that".

Assisting CPC is EV1’s executive director Michael Bourguignon — the project manager during the development of Syrah’s project — who has built a team loosely based on the same team he worked with at Syrah.

Significantly, when EV1 shows the workings of its updated feasibility studies to financiers it will be providing reputable costings which financiers will be a lot more comfortable making financing decisions off of.

So what does the Front End Engineering Design (FEED) contract cover?

The FEED covers all of the design works centred around EV1’s processing plant and all of the associated non-processing infrastructure.

In yesterday’s announcement EV1 specifically confirmed that the scope of works would include the "evaluation of opportunities to improve plant design and optimise and update estimated capital expenditure".

This will come together to finalise EV1’s mine layout so that an updated upfront CAPEX figure can be worked out using inflation adjusted costings.

The simple fact is that financiers would be less willing to finance EV1’s project using 2020 numbers. So the updated design/costings should improve EV1’s ability to introduce the project to these potential financiers.

The ultimate goal for these works will be to incorporate the already identified optimisation measures into the project's design to improve project economics.

EV1 explained one of the key design changes that will be incorporated into the FEED studies which will work towards improving economics and reducing the project’s carbon footprint. That change is the removal of a tailings storage facility and dry stacking of tailings from the current mine design.

EV1 said this would be done by including a water storage dam instead, which would have a much smaller footprint so could be built for a lower upfront CAPEX cost.

Not only does the redesign reduce the upfront CAPEX requirements for EV1’s project but would also cut ongoing sustaining costs.

This is likely to be one of many different optimisation initiatives EV1 integrates into its updated FEED studies.

In summary, we think the market is underestimating the significance of this appointment primarily because of the implications it has on project financing.

The FEED studies will form the basis for updating EV1’s CAPEX calculations.

With the study expected to be completed in September 2022 EV1 will have a detailed, accurate and importantly an up to date schedule of all the upfront capital costs required to build its mine.

At the same time, the updated FEED gives EV1 the opportunity to incorporate both ESG/economic optimisation initiatives that we hope will vastly improve the overall project economics.

What do we expect to see the FEED deliver?

We have seen a common theme across all of the junior mining companies with development ready projects this year.

Almost all that have updated their feasibility studies in line with 2022 pricing of capital equipment have seen upfront CAPEX and ongoing production costs go up.

Even though we think EV1 has scope to improve its project economics with the updated DFS later this year, we expect to see increases in the upfront capital costs of building its project and would not be surprised to see the operating costs also increase.

We think the market will be pleasantly surprised if the company can cut any of these costs.

With the 2020 DFS showing an NPV of US$323M and EV1 only trading at a market cap of A$48.5M, regardless of the outcome we think that EV1’s valuation is still lagging the potential of its project.

As the above peer market cap comparison chart shows, there’s a gaggle of peers trading at valuations much higher than EV1.

We have Invested in EV1 to see it climb up in these valuation rankings.

What’s next for EV1:

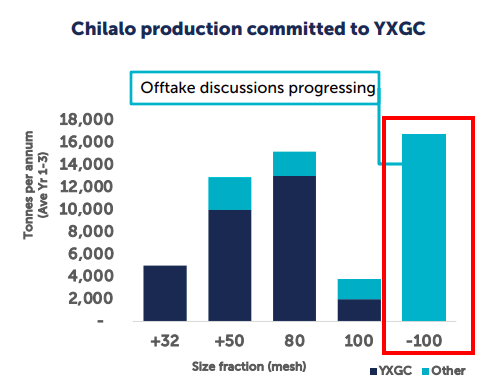

Offtake agreement for fine flake graphite 🔄

A corporate presentation in early May revealed that EV1 was still in discussions with other interested parties with respect to offtake agreements on the fine flake graphite production.

Fine flake graphite is mostly used in the manufacturing of battery anodes and so we suspect that EV1 won’t have any issues getting an offtake agreement over the line on this front.

This portion of its resource represents ~35% of EV1’s life of mine production with the coarse flake higher value graphite already under an offtake agreement with YXGC.

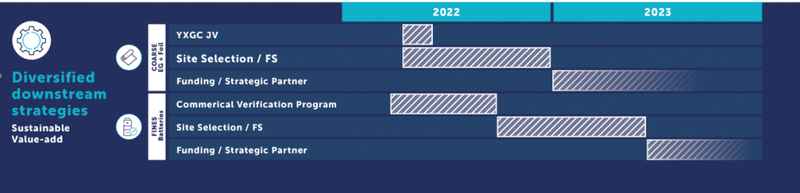

The image below helps visualise what is currently under offtake agreements and what isn’t.

Framework agreement with the Tanzanian Government 🔄

EV1 is currently in discussions with the Tanzanian government over a "framework agreement". Once signed, this will provide fiscal and regulatory certainty to EV1 and to potential financiers.

Other ASX listed companies like Strandline Resources, OreCorp, and Black Rock Mining have already managed to sign these agreements and we have seen BHP and Barrick spend $50M and $60M respectively on projects in Tanzania.

As these agreements provide regulatory certainty around projects, the market reacts positively to this type of news.

For example, Strandline, which signed the agreement on 14 December 2021, has seen its share price go from ~25c before the agreement to briefly touch all time highs at 51.5c, after which it completed a $50M capital raise.

This is fully understandable as a lot of institutional capital would rather wait for the company to have regulatory rules in place before investing.

Once EV1 gets a framework agreement signed with the Tanzanian government, the company will then become an attractive opportunity for a whole heap of new investors which we hope will mean an increase in the company’s share price.

Updated Definitive Feasibility Study (DFS) + final investment decision (FID) 🔄

EV1’s 2020 DFS shows an NPV of US$323M with a 3.4 year post tax payback period based on total capital expenditures of ~US$87M to get the mine into development.

The FEED work that the newly appointed contractor will be doing will feed into an updated DFS later this year.

With the recent inflation news, as we mentioned, capital costs of building the mine are likely to be higher now versus when the DFS was done (2020). So we suspect the CAPEX figure will be higher when the updated DFS is released.

The importance of getting this work done is more about being able to secure financing partners who will want to see updated estimates for capital costs and would be less likely to finance a project based on 2020 estimates.

To counter the increases in upfront capital costs, we hope EV1’s upcoming drilling can bring more "near surface" graphite resources into the current mine plan, potentially lowering the costs of mining the ore and bringing overall operating costs down.

This should improve the overall NPV figure, or at the very least, negate the drag any uplift in CAPEX will have.

We covered the upcoming drilling program in a previous note which can be read here: Never miss a chance to improve DFS economics with near surface exploration.

Downstream strategy update 🔄

EV1 is currently looking at building out its downstream strategy via a joint venture (JV) with China based YXGC.

The first venture the JV is focused on is a downstream EU manufacturing plant with both parties involved in the feasibility, construction and operation of the facility.

EV1 plans to provide its graphite, and YXGC its downstream manufacturing technologies.

Most of this is at the scoping stage whereby both companies are looking to find a suitable location for its plant.

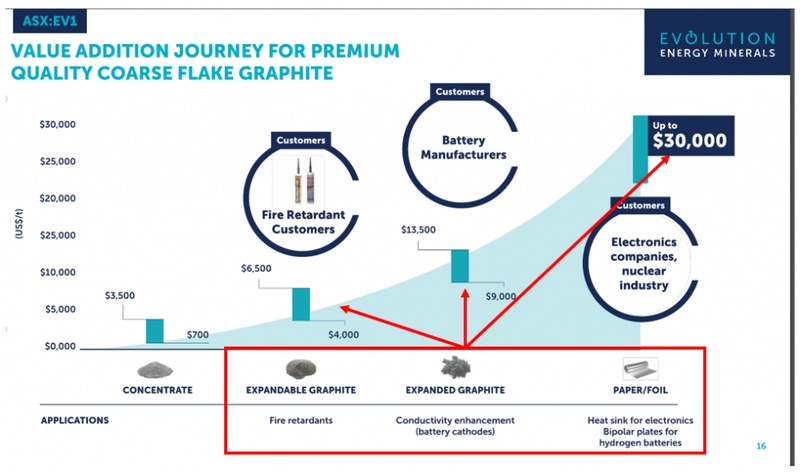

But in the latest presentation EV1 made it clear it would target certain value add products as follows:

- Expandable graphite: Typically sold directly to Western fire retardant customers (up to US$6,500/t)

- Expanded graphite: Typically sold to battery manufacturers as a conductivity enhancement on the cathode side of the battery (up to US$13,000/t)

- Graphite foil:

- Typically sold to electronic device producers for use as a heat sink (up to US$30,000/t)

- Typically sold to hydrogen battery manufacturers for use in the bipolar plates housing the cathode and anode in hydrogen batteries.

One product — the graphite paper/foil that could be used in the bipolar plates for hydrogen fuel cells — has particularly caught our interest.

This interest largely comes as a result of the work Toyota is doing with its internal combustion engines (ICE) .

It is no secret Toyota has been working on hydrogen powered cars for a while now. But recent news about replacing unleaded fuel in ICE engines with hydrogen fuel cells makes us think that automakers will do anything to hold onto the billions of dollars and decades of R&D spent developing ICE engines.

The hydrogen fuel cells that are needed to power these engines require graphite paper/foil - a high value add downstream product that can sell for upto ~US$30,000/tonne.

If we see any adoption of this tech then the demand for graphite will increase and companies who have downstream tech in this space will be the big beneficiaries.

We are watching this space...

Our 2022 EV1 Investment Memo

Below is our 2022 Investment Memo for EV1 where you can find a short, high level summary of our reasons for investing.

The ultimate purpose of the memo is to track the progress of our portfolio companies using our Investment Memo as a benchmark, throughout 2022.

In our EV1 Investment Memo you’ll find:

- Key objectives for EV1 in 2022

- Why do we continue to hold EV1

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.