…and LYN is about to find out.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,401,250 LYN shares and 300,000 LYN options at the time of publishing this article. The Company has been engaged by LYN to share our commentary on the progress of our Investment in LYN over time.

The West Arunta region of WA is an exploration hotspot right now.

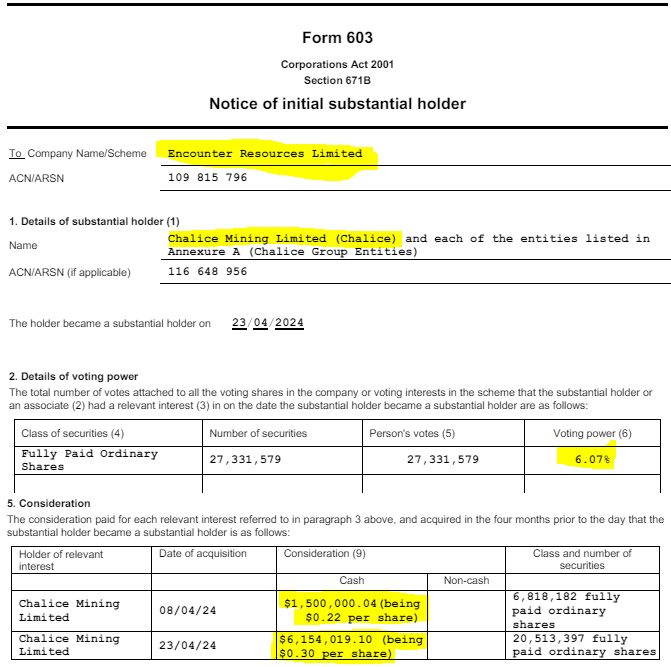

$480M Chalice just bought into West Arunta explorer Encounter Resources.

Juniors drilling in the region are running over 500% in a matter of weeks.

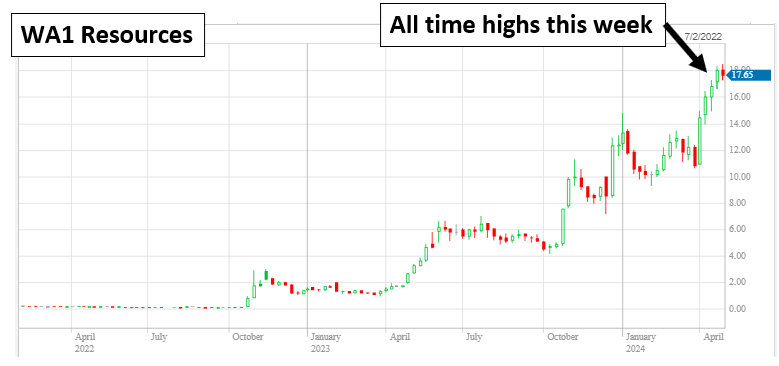

AND WA1 Resources—the company that put the region on the map—is trading at an all-time high.

WA1 hit $18.48 per share a few days ago - up 147x on its pre-discovery 12.5c share price.

The winter drilling season has just started in the region, and a handful of “next WA1” hopefuls are all about to start spinning the drill bit...

Our Investment with ground in the West Arunta is Lycaon Resources (ASX:LYN).

LYN’s plan is to drill its targets in “the middle of this year.”

Which we read as within the next few months.

LYN’s project sits ~90km away from WA1 and has similar geophysical anomalies to the ones WA1 drilled to make its discovery.

Note: Always remember that just because WA1 had big success and a huge share price run, doesn’t mean LYN will do the same. Exploration is risky, lots of things can go wrong.

That being said, we are small cap exploration investors and accept the risk-reward on offer - we are betting on LYN making a discovery and hopefully delivering even a fraction of WA1’s success, which would be a great result.

Great timing, considering the corporate interest in the region from Chalice & the market interest in WA1.

With LYN’s big drilling catalyst only a few months away, another big positive for the company is that it has already locked away a capital raise to fund the drill program.

LYN raised $2.5M at 28c per share, adding to existing cash of $2.46M (at 31 March 2024) which should be enough to get LYN through drilling on its West Arunta projects this season.

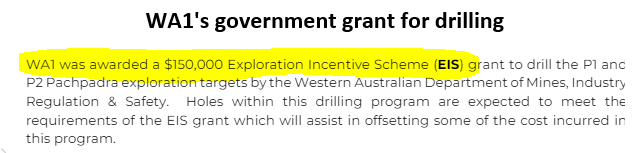

LYN also secured a grant from the WA government to drill its project - interestingly, that was the same grant that WA1 got leading up to its drill program back in 2022.

(Source)

If the drilling comes in, we hope LYN’s share price re-rates much higher than where it is, especially considering its current market cap.

After the capital raise, LYN will have ~53M shares on issue which could add to a rally IF LYN were to make a discovery.

(a low number of shares is desirable because if the underlying value is delivered in the company, the share prices run higher because the created value is split between a lesser number of shares on issue)

We think that was one of the key reasons for WA1’s share price rally - for context, WA1 had ~43M shares on issue when it made its discovery.

At the capital raise price (28c per share), LYN’s market cap is ~$15M, compared to the region's blue-sky valuation, WA1’s market cap, which touched ~$1.1BN earlier this week.

Latest in the West Arunta region

West Arunta appears to be attracting more and more investor interest as time goes by.

Recently, a few smaller companies drilling in the region started running.

Rincon Resources started drilling in February, and its share price has gone from ~2c per share to a high of ~10.5c per share earlier this week - up over 500%...

CGN Resources also started drilling, and its share price was up ~100% over the last few weeks.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think the reason for the sudden investor interest in the region was the Chalice buying in Encounter Resources.

Chalice paid ~$7.5M for shares in Encounter, signaling to the market that corporates are interested in any explorer with ground in the region looking to make discoveries.

Another reason could be because WA1’s valuation hit an all time high this week.

WA1 hitting over $18.84 per share which gave the company a market cap of ~$1.1BN.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The WA1 share price rise means a lot of money was made investing in an explorer in the region who actually managed to make a discovery.

Usually when that much money is made so quickly, investors start to look for the repeat story (“ the next WA1”).

As long as WA1’s valuation stays high we expect more and more capital to flow into the juniors in the region.

Especially considering a lot of the juniors were trading at sub $10M market caps before the last few weeks.

Our view is that as LYN approaches its drill program in the middle of the year, as long as there is positive momentum in the region & WA1’s valuation holds up, LYN’s share price could re-rate into drilling (and fingers crossed into a discovery).

The WA1 story - what success looks like for LYN -

The poster child for success in the West Arunta is WA1.

WA1 made its discovery in October 2022.

At the time its share price was ~12.5c per share...

Post discovery the share price quickly ran to ~$3 per share.

Over the next 18 months, WA1 has kept delivering monster drill hit after monster drill hit and just this week hit an all time high share price of $18.48 per share.

The market cap briefly touched ~$1.1BN, which gives a good indication of what success might look like for the juniors looking to replicate WA1’s success.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

This is the kind of story and result every small cap exploration investor invests for.

LYN to drill similar targets to WA1

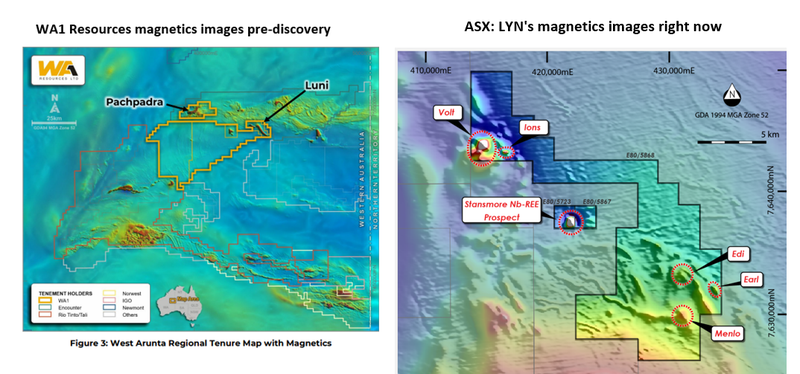

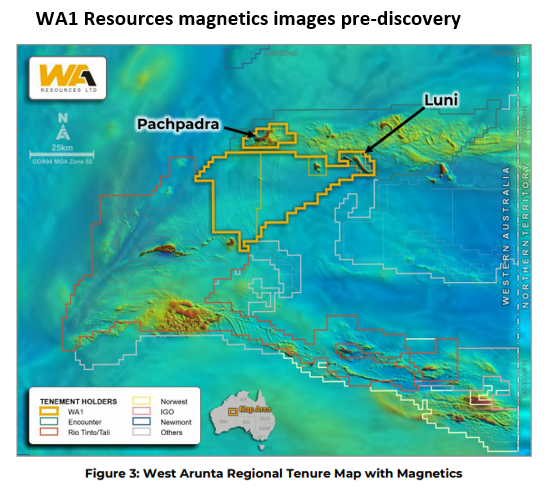

At a very high level, LYN’s drill targets are based on geophysical surveys.

LYN has a set of geophysical anomalies - similar to the ones WA1 drilled before it made its Luni discovery.

Here is a side-by-side of LYN’s projects compared to WA1 Resources (pre-discovery) - notice both had distinct geophysical “hot spots”:

(Source)

(Source)

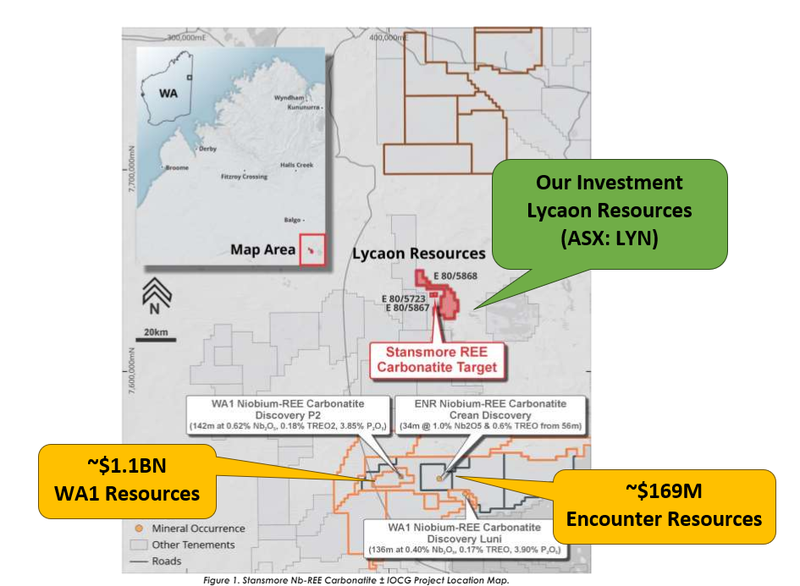

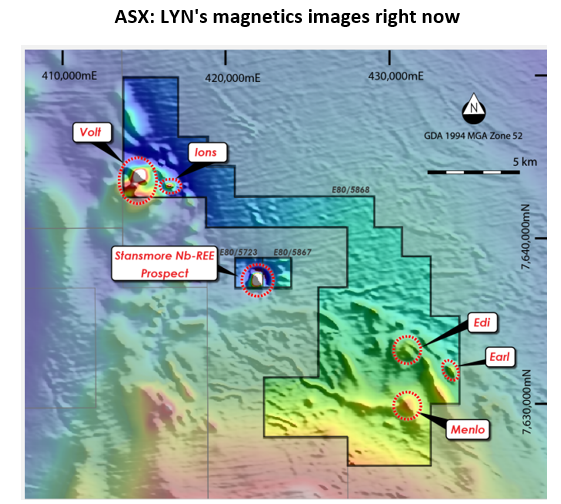

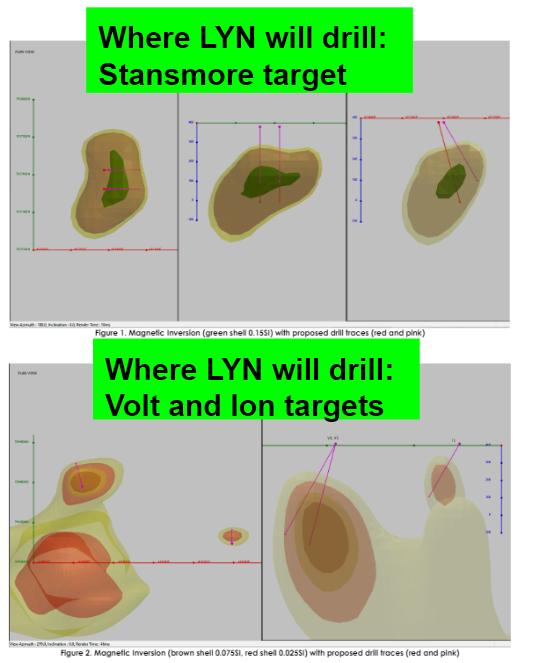

LYN has also spent the last ~6-9 months refining the targets to better plan its drill program.

Here is the latest set of images showing LYN’s targets and where it plans to drill:

At the end of the day, we are Invested in LYN to see it try and replicate some of WA1’s success - that forms the basis for our LYN Big Bet which is as follows:

Our LYN “Big Bet”:

“LYN’s share price re-rates by over 1,000% off the back of a new discovery and the definition of a deposit significant enough to move into development studies”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our LYN Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

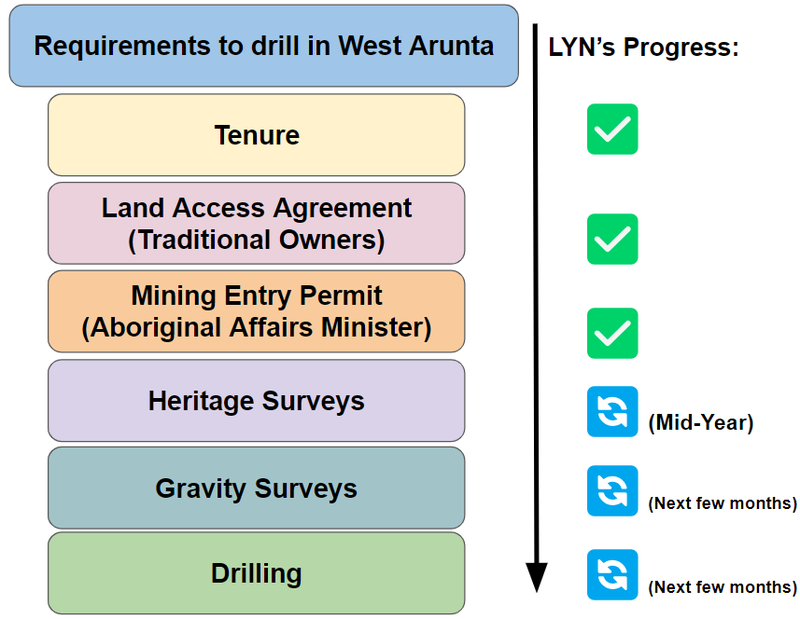

What’s next for LYN in the West Arunta?

What could go wrong?

The key risks in the short term is “Delay risk” and “Permitting risk”.

Blowouts in timelines could mean LYN continues burning cash with the drill program being delayed, the longer the delays the lower LYN’s cash balance is likely to be by the time drilling comes around.

And also miss the opportunity to drill during a window when interest and capital flow into the region is heating up.

Ideally, LYN would be going into its drill program with as much cash as possible in the bank so that the market doesn’t start pricing in another capital raise.

As a result, delays could put pressure on LYN’s share price in the short term.

The second risk is permitting.

There is always a chance the heritage surveys take a lot longer than first anticipated and/or throws up issues that may take a long time to resolve.

If LYN has any issues getting heritage surveys completed there is a risk the drill program gets delayed even further.

To see more risks to our Investment in LYN, check out our LYN Investment Memo here.

Our LYN Investment Memo

Below is our LYN Investment Memo, where you can find the following:

- Key objectives for LYN for the coming year

- Our LYN Big Bet

- Why we are Invested in LYN

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.