A busy week...a trip to Perth, WA lithium is hot, cap raises and more M&A

Published 18-NOV-2023 13:00 P.M.

|

13 minute read

We have just spent a few days in Australia’s “small cap exploration capital”, Perth, Western Australia.

We met brokers, corporate advisors, investors and managing director’s of existing (and potential) Portfolio companies.

Small cap investors know that Western Australia is where most of the exploration deals get done.

Compared to the last two years, the average mood in the industry has suddenly become ... more positive.

There are a couple of small cap winners out there and people are starting to remember that small cap investing can actually be fun... and small cap stock prices are, in fact, capable of going up.

In all discussions, Western Australian lithium is the hottest sector in the market.

Some quick examples of activity in the WA lithium space in the last ~6 months:

- AZS up ~1,400%

- RDN up ~1,700%

- TG6 up ~700%

- WC8 up ~ 2,600%

- Liontown resources takeover offer

- Azure minerals takeover offer

- Allkem merger with Livent

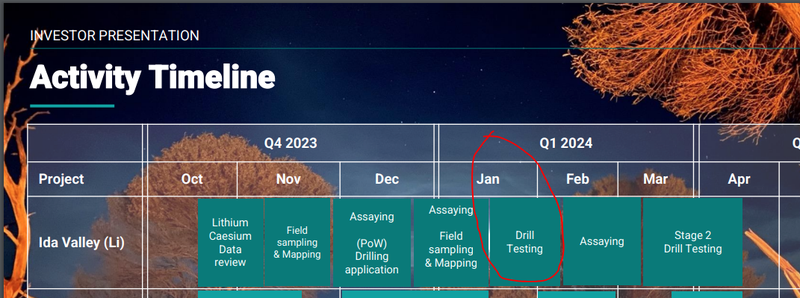

Ash Hood from TechGen Metals (ASX:TG1) was by far the most excited MD we spoke to during our trip.

Ash was too busy to meet us in person because he was on the way to the airport to fly to TG1’s Ida Valley project where they have just found some lithium in soil samples that were collected in past gold exploration work.

They are going to do some sampling and mapping in the areas of interest, hopefully leading to some new WA lithium drill targets.

According this latest TG1 preso they are planning to drill in January:

(source)

TG1 is currently in a halt for a capital raise and is expected out of halt by Tuesday.

We are taking a pretty big swing at this TG1 placement, given the heat in the WA lithium sector, TG1’s tiny market cap (~$5M) and drilling expected in January.

Earlier this month we wrote that TG1 was low on funds which meant that on-market buying may have been limited in anticipation of an incoming cap raise (as is the rule of thumb for stocks that don’t have much cash in the bank).

Next week we should see TG1 come back online with a replenished war chest to execute on their Ida Valley lithium project and drilling timeline.

(Important to note that small cap exploration is highly risky, and just because some WA lithium explorers are performing well does NOT mean that TG1 will do the same)

We caught up with our uranium explorer Haranga Resources (ASX:HAR)’s Managing Director Peter Batten and heard about the recently announced auger drilling campaign in Senegal.

Peter from HAR gave us a detailed history of a few uranium companies and how they came about, the people involved and the intricacies of soil sampling from termite mounds - one thing is for sure Peter knows a LOT about uranium exploration.

If you ever manage to corner him at a conference ask him to tell you the Bannerman story - he was the MD of Bannerman Resources which was crowned the best performing stock on the ASX in 2006, during the last big uranium price run.

HAR and our two other uranium investments OKR and GTR generally move in lock step with uranium sentiment and the uranium price.

The uranium price looks close to hitting $78/lb which is higher than when we first started writing about a potential U price run back in September when it was ~$65/lb, so it’s still going up...

On the biotech side, we went to visit Emyria (ASX:EMD) managing director Mike Winlo and had a tour of the world’s first private clinic for MDMA treatments for mental health.

EMD's primary area of focus is on psychedelic assisted therapies using MDMA, ketamine and psilocybin to treat difficult mental health problems in innovative ways.

EMD is the first mover in the space globally, taking advantage of Australia being the first country in the world to legalise the use of psychedelics (MDMA, psilocybin) for treatment of mental health disorders.

(we are still baffled at how or why Australia is the first country in the world to legalise this, but it is)

EMD is working on genuinely exciting and ground-breaking treatments for mental health and is the first company in the world to be able to trial, develop and refine a “private commercial clinic” model to scale up delivery of these innovative new treatments for broader consumers.

It was very cool to take a tour of this world first clinic, and we also got to spend some time with Dr Jon Luangharne, who is the psychiatrist heading up the program.

(here is our launch note on EMD)

While the mood was good in WA lithium, uranium and biotechs, most other parts of the small cap market are still pretty grim.

Many small cap companies are nearly out of cash and have been holding out for the market to come back to life.. which hasn't happened just yet... even though this week did have a “start of a small cap santa rally” vibe to it...

Either way, a lot of small cap companies will need to take the window from now until around December 15th (when the market unofficially shuts down until February) to raise capital.

And with market sentiment (and share prices) so low, the terms of the cap raises aren't going to be pretty...unless of course you are the one investing in the cap raise... in which case they are awesome.

Steep discounts to already low share prices PLUS 1 for 2 or even 1 for 1 oppies are the norm at the moment to entice investors out of their “risk off” mentality and to cough up some dough to a small cap explorer.

It feels like there is a bit of positive sentiment coming into the market which will hopefully last into the Christmas break - and possibly form a base for a better 2024 for ASX small caps.

We will look to add around three new portfolio companies before Christmas - hopefully at a bear market entry point and right into a 2024 sentiment lift in the small cap markets.

And then fingers crossed 2024 is a more positive time in the market (keeping in mind it could absolutely still get worse from here, and for longer than you think).

So where did all the small cap investors go over the last two years anyway?

And what will make them come back?

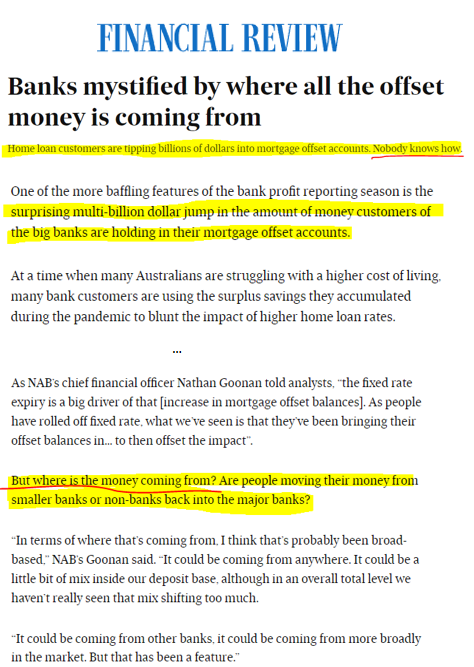

We saw an interesting article this week, where the big Australian banks were having a whinge that lots of people with home loans are putting more and more money into their “loan offset accounts” to reduce their monthly interest payments.

A “home loan offset account” is basically a savings account where the amount of money that you keep in that account is deleted from your home loan amount when the bank calculates your monthly mortgage interest payment.

The more free cash you park in a loan offset account, the less your interest repayments are.

A pretty good place to park all your spare cash after 13 interest rate hikes...

(source)

So the banks are “mystified” as to where all this money ($ billions of dollars) that people are putting into offset accounts is coming from...

Well we know where SOME of it is coming from.

We reckon that a good chunk of this has come from people who have been belting out their small cap stocks into thin buy depths over the last 2 years.

If your interest rate payments have rocketed, and your small cap stocks have been going down, down then down some more, most rational people would likely come to the conclusion that this money should be pulled out of the small cap market and be better put to work reducing their loan payments by sitting in an offset account.

This sounds like a great idea - the problem is that when everyone has this same great idea at the same time, they all start pressing the small cap sell button and small cap stocks get smashed as everyone rushes to free up money for their offset account.

So now we have hoards of cash sitting in offset accounts and a bunch of bombed out small cap stock prices trading at multi-year lows.

(we have increased the pace of investing in small caps during this time in our “2023 bear market planting season”, even though it feels VERY counter-intuitive)

Many small cap stocks have made great progress over the last two years, but people still feel their money is better placed in their offset account, so there are almost zero on-market buyers for small cap stocks.

Even cap raise terms for small caps trying to raise money have to be extra juicy to prise money out of the coveted offset account (steep discounts and free oppies) which is the trend we are seeing now (and hence we are participating in more cap raises than usual).

There are two things that we think will start moving money out of offset accounts and back into small cap stocks.

The first is people seeing small cap stocks go up.

Winners have been few and far between lately so why would anyone want to put cash to work in a small cap stock that keeps going down when it could be shaving thousands off their monthly mortgage payments instead?

If the small cap market can deliver a few highly visible mutli-baggers that everyone sees, suddenly the POTENTIAL returns in small caps become better than sitting in an offset account (albeit almost infinitely riskier).

This could attract some money back from offset accounts back into the small caps, starting with the early risk takers.

(this is what has happened in WA lithium stocks)

The second and obvious one is any sniff of interest rates coming back down.

Once sentiment of interest rate cuts takes hold, early risk takers will be attracted back to buying small cap stocks, either by attractive cap raise terms or buying on market at mutli-year lows.

When small cap share prices are as beaten up as they are now, they can usually show decent price rises on a small amount of buying.

These price rises will be noted by people who have the stocks on their watchlist, and possibly encourage them to also put on a small bet.

The cycle of positivity and buying continues and then we are suddenly back to normal or bull conditions.

So much like everyone selling at the same time to free up money to put in their offset account is a self perpetuating cycle, so is the opposite when everyone decides to cycle back into small cap stocks.

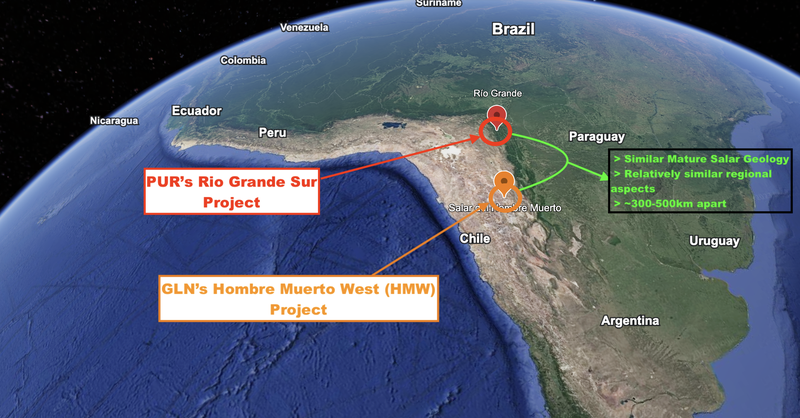

Glencore signs Argentia lithium Brines offtake

(Source)

This week, ~$250M capped Galan Lithium (we aren’t investors in Galan) announced a surprise 5-year binding offtake with ~$115Bn capped Glencore PLC (LSE: GLEN) for Lithium Chloride and/or Lithium Carbonate product from its Hombre Muerto West project in Argentina.

This is of interest to us because of our Investment in $30M capped Pursuit Minerals (ASX: PUR), who also have a lithium brine project in Argentina, with a maiden JORC resource of 251.3kt LCE (based only on historical shallow drill data) and drilling is starting in the coming weeks.

Like many other sectors, lithium brines have been a bit on the nose over the last 12 months, with many lithium brine stocks trading at 12 month lows.

We hope that much like the WA lithium sector had a rocket put under it when the big players starting fighting over WA lithium assets, that mining big-dog Glencore snapping up all of Galan’s phase 1 lithium brine production in Argentina could start re-igniting interest in South American lithium brines.

And in our portfolio company PUR.

Glencore is a global powerhouse of natural resources mining and trading commodities, it holds interests in over 35 countries and regions, having a highly diversified portfolio of copper, nickel, alumina and coal just to name a few.

According to the Definitive Feasibility Study (DFS) by Galan on its project - a mature Salar asset located in the “lithium triangle” - Phase 1 of development will include the production of approximately 5.4kt of lithium carbonate equivalent (LCE) in lithium chloride concentrate, per annum.

Our Argentinian lithium Investment PUR, holds an advanced lithium asset in Argentina, the Rio Grande Sur project, located in South America’s “lithium triangle” which is home to ~50% of the world’s lithium production.

PUR already has a maiden JORC resource, prior to any drilling, at its lithium brine project of ~251.3kt (inferred) lithium carbonate equivalent (LCE).

Both GLN and PUR’s assets located in Argentina and have similar geological and geographical aspects, but both have parallel mature Salar structures:

We believe that PUR is undervalued when compared to its larger, more advanced peers and with Glencore sniffing around for South American lithium, this opens opportunities for similar offtake deals with other global resource majors.

Galan’s binding offtake also comes with a Financing Prepayment Facility offered by Glencore to GLN. The facility is set to provide US$70-100M for the production and development of Phase 1 of the HMW project, subject to due diligence conditions by Glencore.

Not only is this binding offtake an opportunity for Galan to transition from a Lithium developer to a producer, but a promising vote of confidence in Argentine lithium brine quality and potential by a global resource heavyweight.

While it’s only the one deal in the region for now, hopefully (for us and PUR) this is the start of a “WA lithium” style battle of the big dogs for control of lithium supply in the region.

What we wrote about this week 🧬 🦉 🏹

GTR has commenced Uranium drilling campaign. Uranium price keeps going up.

On Wedneday, GTR kicked off its latest round of drilling at its Lo Herma project, which holds 5.71 million lbs of GTR’s resource base.The drill program is for 26 holes across ~4,600m - the first phase of a much larger permitted program for ~68 holes. Uranium macro fundamentals are as strong as they have ever been, 3rd U bull run?

88E heading to Africa on frontier oil hunt - following Shell and Totals 11 billion barrel lead

88 Energy has just farmed into a massive 18,500 km2 onshore acreage in Namibia (this is 12x larger than its current Alaskan acreage). Namibia has been dubbed the world's most exciting oil and gas province.

Graphite is Back. SGA preps more samples to repeat 99.99% battery grade test success.

On Monday, SGA announced that bulk graphite concentrate samples had been sent off to testing labs for “spheroidization, purification and battery testing”. We think graphite could be back in a big way.

Quick Takes 🗣️

EXR: Daydream-2 Progress Update

TYX: More Intersections of Spodumene-Bearing Pegmatites at Muvero

HAR: Haranga to probe Senegal uranium project anomalies

EMN: Euro Manganese Produces Sulphate Product

TEE: Section 31 Deed Executed for Northern Territory gas project

Bite sized summaries of the latest mainstream news in battery metals, biotechs, uranium etc: The Future Money: https://future-money.co/

⏲️ Upcoming potential share price catalysts

Updates this week:

- TYX: Second round of drilling at lithium project in Angola

- This week TYX announced more interceptions of high-grade Spodumene bearing pegmatites at the Muvero prospect in Angola. Read more in our Quick Take here.

- EXR: Daydream-2 appraisal well, QLD

- After the spudding of the Daydream-2 well earlier this month, EXR recently announced to the market that it had reached a depth of 856m of the total ~4,200m planned. See our Quick Take on this news here.

- NHE: Drilling two targets at its helium project in Tanzania (Q4, 2023)

- Final results are expected in a few weeks for Mebele-1. This week, NHE announced that the Mebele-2 well has been spudded and drilling commenced. See the ASX announcement here.

- IVZ: Drilling oil & gas target in Zimbabwe, Mukuyu-2 (Q3, 2023)

- Sampling operations for Mukuyu-2 set to recommence following minor delays due to tool failure. Read more in the ASX announcement here.

- 88E: Flow test well, Alaska (Q1, 2024) & Government approvals for gas project, Namibia (Q1, 2024)

- No news on the Alaskan flow test well this week. However, 88E has farmed-in into a significant onshore exploration project for oil and gas in Namibia. We wrote a note on it, read more here.

No material news this week:

- PUR: Drilling its Argentine lithium project in Q4-2023.

- SLM: Assay results from drilling at its Brazilian Lithium project.

- DXB: Interim Analysis of Phase III Clinical Trial on FSGS (March 2024)

Have a great weekend,

Next Investors

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.