Tiny Medical Cannabis Stock BOD Has Started Two Clinical Trials - We are Hoping for a Re-rate on Results

Disclosure: The owners of Wise-Owl, S3 Consortium Pty Ltd, and Associated Entities, own 500,000 BOD shares at the time of publication. S3 Consortium Pty Ltd has been engaged by BOD to share our commentary on the progress of our Investment in BOD over time.

Our cannabis investment, BOD Australia (ASX:BOD) is pursuing clinical trials for two large markets that could be the keys to unlocking a long awaited re-rate.

BOD dosed the first patients for the following trials in the last month:

- Insomnia (Phase IIb)

- Long-COVID (Open label, "Proof of Concept")

We first Invested in BOD at 50c in early 2021 when medical cannabis stocks broadly were performing well. So far, this one has not turned out as we hoped as regulatory reform around the world has stalled, especially in key markets like the US and the UK.

Cannabis use spiked during the pandemic and consumer demand hasn’t waned.

The problem is getting quality products with proven benefits into the hands of these consumers - something BOD is aiming to do with these two trials.

With the share price now sitting at 14 cents, and a ~$14M market cap, BOD trades at around twice last year’s revenues ($7.43M), and has over $4M cash in the bank as of 31 March 2022.

BOD is a long-term hold for us, and whilst we aren't happy being significantly underwater with our original Investment, we’re pleased it is pursuing these clinical trials, as we hope they can deliver a decent value uplift for the stock.

If market sentiment returns to the cannabis sector, our conviction is that BOD is well placed in the market to capitalise on renewed investor appetite.

Part of our reasoning here is that another ASX company (Incannex Healthcare) is generating zero revenue but doing a number of cannabis clinical trials — it is capped at more than $600M. We will go into more details on that further down.

The market appears to reward clinical trials in the medical cannabis space, and we are looking forward to seeing if the market will reward BOD over the coming 12 months.

As we’ll discuss today, BOD’s increased focus on R&D (via these two clinical trials) is important to their future success.

For one, we’re looking for a marketing coup created by clinical success. In effect, we think successful clinical trials would be the calling card BOD needs to grow sales enough for the market to notice it again.

Alternatively, the clinical trials could give BOD the intellectual property it needs to justify a higher valuation relative to its existing strong revenues.

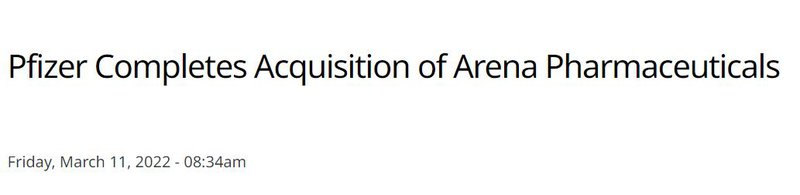

The last 12 months has seen two notable cannabis acquisitions by Big Pharma companies:

- March 11, 2022 - Pfizer acquires Arena Pharmaceuticals for US$6.7B

- May 5, 2021 - Jazz Pharmaceuticals acquires GW Pharmaceuticals for US$7.6B

That’s a total US$14.3B (~$20B) poured into companies that have cannabis products with successful clinical trials.

We’ll dive into the significance of those deals shortly.

But for now, these deals underline just how important clinical trial success is for BOD - something which we think could eventually see it valued at multiples of its current market cap (~$14M).

The trials also provide the market with clearly defined catalysts beyond simple revenue growth figures.

With these catalysts down the track, we’re taking the opportunity to launch our BOD Investment Memo.

This is a short, high-level summary of why we’re invested in BOD, what we expect BOD to achieve in 2022, risks and our investment plan:

With a reinvigorated R&D pipeline, we’ll dissect BOD’s prospects as follows:

- BOD, its revenue, and the cannabis market

- More on BOD’s two clinical trials

- Why money is flowing to cannabis companies with Intellectual Property (IP)

- Introduce our 2022 BOD Investment Memo

BOD, its revenue, and the cannabis market

BOD is primarily a CBD company with a medicinal arm and a health and wellness arm.

- Medicinal Cannabis — focused on sales of its established MediCabilis product in Australia and the UK;

- CBD Wellness —under which all of BOD’s 30+ products are licenced to Swisse Vitamins’ H&H Group. These products are sold and distributed in the UK, Italy, Netherlands, Australia and the USA.

CBD is a specific cannabinoid which doesn’t get you "high," but has been shown to have various health benefits.

The key for BOD is to prove these health benefits, so that they can better sell their products.

Since listing in 2016, BOD has broadened its established sales network from Australia and the UK and is expanding its reach into multiple international markets including the USA, Italy, France, and the Netherlands.

BOD is backed by its partnership with multinational health and nutrition giant, the Health and Happiness Group (H&H) - the owner of Australia’s largest vitamin and supplements brand, Swisse. H&H is also BOD’s biggest shareholder through its innovation arm NewH2 which holds a 14.03% stake.

With its extensive global distribution network, H&H provides a substantial competitive advantage for BOD. It means they can get their products into a large number of outlets across the globe.

For BOD, last year was all about continuing to grow sales.

That said, the market clearly didn’t care much for BOD’s revenue and sales growth, nor its expansion. The share price dropped from a high of 50 cents (when we first Invested) in March 2021 to less than a third of that today.

Revenue has continued to grow every year since listing in 2016, although BOD is yet to deliver a profit.

However, we don't think that's the sole reason for the share price taking a hammering. It could be due to a number of factors and we suspect that a big reason for BOD’s lacklustre market performance over the past year can (at least partially) be accounted for by weak sentiment towards cannabis stocks.

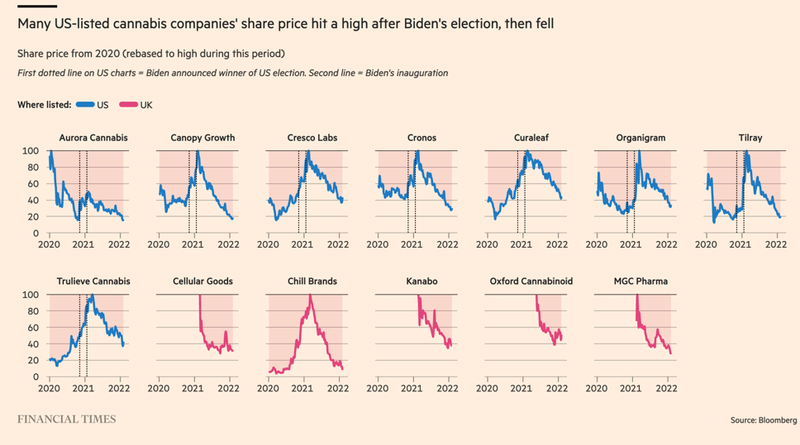

As you can see below, this sentiment has a political flavour:

The election of Joe Biden in the US was greeted by big moves upwards for a broad swathe of cannabis stocks. Cannabis legalisation was on everyone’s lips and it was meant to be part of a global push that would increase access to legal/medicinal cannabis products.

The UK was also meant to be a hub of regulatory reform.

However, as time has shown, there was a mismatch between initial market expectations surrounding ASX-listed cannabis companies (and cannabis companies globally) vs the realities of running businesses as legalisation/regulatory reform legislation stalls.

For example, the benchmark ETF for US based cannabis stocks has a strikingly similar chart to BOD:

The bear market for cannabis stocks, and for BOD itself, has resulted in the company’s market cap dropping to just ~$14M.

Or to put it another way, BOD trades at around twice last year’s revenues ($7.43M), with over $4M cash in the bank as of 31 March 2022.

In its most recent quarterly, BOD got within touching distance of a cash flow positive quarter, with an operating cash outflow of $290K.

Strong sales aren’t enough for BOD though, which is why a peer comparison with Incannex Healthcare reveals what BOD needs to do.

Incannex Healthcare is capped at ~$600M and has no revenues.

The difference seems to be that Incannex is viewed more as a biotech with a competitive moat built around IP, particularly via clinical trials.

Incannex has a number of cannabinoid formulations in the clinical trial pipeline - one for sleep apnoea, one for concussions and another for a range of different types of inflammation.

Clearly, the market views the Intellectual Property (IP) generated by clinical trials as valuable.

It’s one thing to sell your cannabis product, but it's an entirely different ball game if you can prove that a specific formulation of your cannabis products has tangible medical benefits.

More on BOD’s two clinical trials

Whilst BOD remains a high risk small cap stock, we think a turnaround may be on the cards and here’s why...

BOD is progressing two clinical trials now (first patients were dosed for both in the last month):

- Insomnia (Phase IIb)

- Long-COVID (Open label, "Proof of Concept")

There are sizable markets for both products if proven safe and effective. The barrier that BOD needs to knock down is the reticence of medical professionals such as pharmacists and doctors for providing these products.

In addition, while typical new medical treatments can take a decade or so to reach the market, the CBD treatments that BOD is progressing could both be available to the masses next year.

The products BOD is using for these trials are already in the market - what BOD needs to do now is show that they actually work for patients.

The trials represent a two-pronged approach to growing market share - getting a lower dose product through the regulatory hoops in Australia - and growing the potential patient base in the UK for a much higher dose product.

Again, the successful completion of these trials provides clear catalysts for the market.

The insomnia clinical trial is a Phase IIb trial using BOD’s Schedule 3 (pharmacist only) CBD formulation (lower dose).

The trial will run for a total of 12 weeks, with approximately 200 participants.

This follows the Therapeutic Goods Administration’s (TGA) landmark decision in December 2020 that down-scheduled CBD to a Schedule 3 from a Schedule 4 (Prescription Only Medicine).

This regulatory move paved the way for CBD products to be purchased as over-the-counter treatments at pharmacies from July 2021.

Since that decision, there are still no TGA-approved CBD products that pharmacists can prescribe. But BOD hopes to pioneer change in this area.

BOD anticipates that if the Phase IIb trial goes well, they’ll be able to register it with the TGA and eventually get it added to the Australian Register of Therapeutic Goods (ARTG), meaning it could be sold in pharmacies without a prescription.

There are several ASX-listed cannabis stocks out there, but BOD, alongside EcoFibre and Cann Group, are the only three (to our knowledge) currently progressing CBD products that could be available as of next year.

And while some of Inncannex’s formulations are combinations of CBD and other drugs, Inncannex is not pursuing a CBD-only Schedule 3 product.

This leaves an opportunity for BOD to quickly become a market leader in Australia.

BOD’s trial could help build the confidence of pharmacists to recommend BOD’s product, open up the $250M Schedule 3 CBD market for BOD in Australia and, importantly, provide data for product registration with as in: the US FDA and European regulatory bodies.

That last bit could be important down the track.

Meanwhile the Long-COVID study is being done in the UK using BOD’s MediCabilis product (a high dose 5% pure CBD oil).

As this trial is an open label clinical trial, participants know what treatment they are getting. It’s a six month daily regimen with 30 participants.

We’d term this trial a "Proof of Concept" trial that is about expanding the ability of doctors to prescribe BOD’s product.

It’s being run in collaboration with Drug Science UK and is designed to build the evidence base around prescribing medicinal cannabis. If the results are good, then doctors would feel more comfortable prescribing MediCabilis to Long-Covid sufferers.

You could also imagine the media headlines around a treatment for Long-Covid if a trial were successful.

We expect BOD’s product to be proven as safe - and any improvement in symptoms across the majority of the 30 participant cohort we’d call a strong success.

Even symptom improvement in a smaller portion, enough to warrant follow up studies, would be acceptable.

CBD remains in a legal grey area in the UK. It’s widely available at shops but the Food Standards Agency has put the brakes on new product applications recently:

BOD has a range of products approved already, these are the CBD wellness products, but MediCabilis is a prescription only medicine.

So if it is to grow market share in the UK (particularly its high dose medical cannabis sales), it will certainly help if they can prove the MediCabilis product alleviates symptoms of Long-Covid.

The UK was one of the hardest hit countries at the peak of the pandemic and there are 1.8M people with Long-Covid in the country .

Intriguingly, the pandemic coincided with a massive boom in the UK CBD market. According to one report , the UK CBD market hit £690M ($1.2B) in sales in 2021, almost doubling its 2019 figures and is on course to hit £1B ($1.77M) by 2025.

This makes the UK the second largest consumer cannabinoid market after the US.

To our knowledge, it would be one of just a handful of clinical trials recruiting in the UK trying to link CBD and Long-Covid.

As a result, we think BOD’s UK clinical trial is the more interesting of the two trials, given what we know about the UK CBD market and the opportunity there.

This would help BOD legitimise the CBD industry in the UK and accrue the benefits from that.

But if BOD proves that its specific formulation works for a widely suffered condition (Long-Covid) we think it could quickly grow market share in the UK and start to court large commercial partners or become an acquisition target itself.

Why money is flowing to cannabis companies with Intellectual Property (IP)

Here are two recent deals in the cannabis industry that recently came onto our radar.

The first acquisition we want to profile is one specifically related to the UK CBD market:

Before it was acquired, GW Pharmaceuticals was the maker of epilepsy treatment Epidiolex.

In 2018, Epidiolex became the first plant-derived cannabinoid medicine ever approved by the U.S. FDA.

We think GW’s Epidiolex is in some ways similar to BOD’s product - high dose CBD made to the highest standards.

It had sales of over US$500 million in 2020 with analysts predicting significant growth ahead of it .

The first thing that this deal underscores is that not all CBD is the same. There are a variety of products with varying levels of quality and few with clinically proven qualities.

While there are plenty of people that are happy to dabble with CBD formulations of varying qualities - major sales breakthroughs come when it is trusted by medical practitioners.

The second major cannabis deal we want to profile happened just two months ago:

The deal was another monster, with Pfizer forking out a total of US$6.7B ($9.7B) for Arena Pharmaceuticals.

Among other drug candidates, Arena is advancing trials of Olorinab , "an investigational, oral, full agonist of the cannabinoid type 2 receptor (CB2)."

While the Pfizer/Arena deal was not exclusively about their cannabinoid drug, it does indicate that Big Pharma is willing to pony up should the evidence indicate a cannabis treatment is both safe and effective.

With this context in place, we’ve decided to launch our 2022 BOD Investment Memo.

Below is a breakdown of our 2022 Investment Memo for BOD

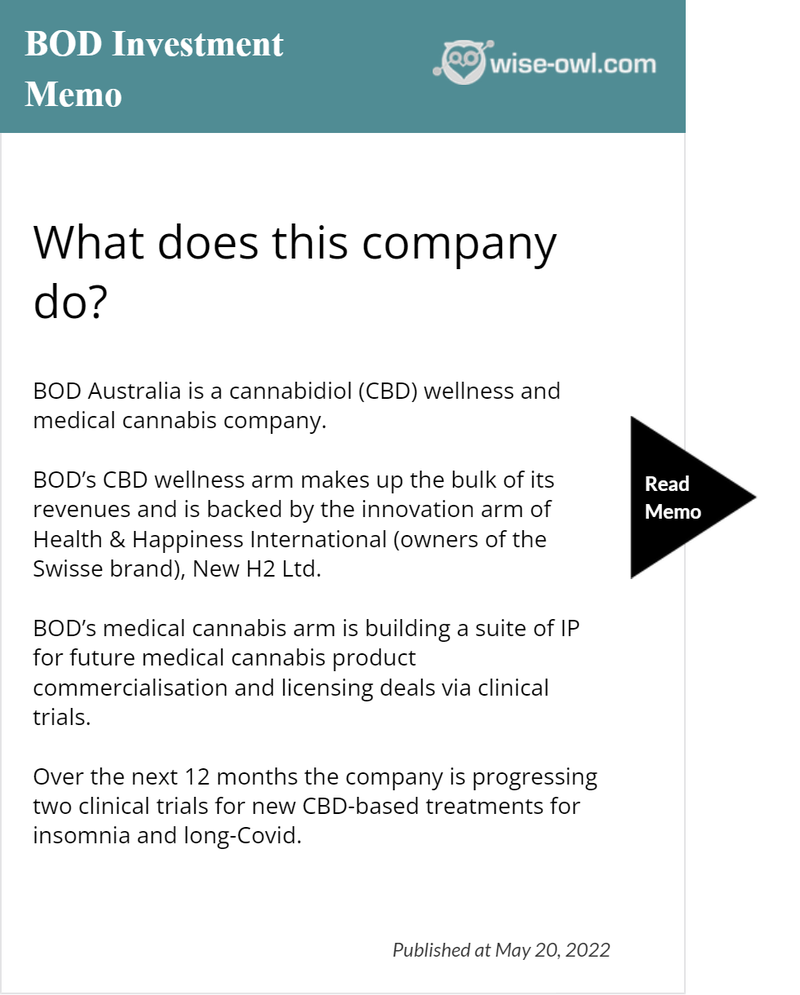

What does this company do?

Here’s our summary of what BOD does:

What is the Macro Theme behind BOD?

This is the macro theme behind BOD:

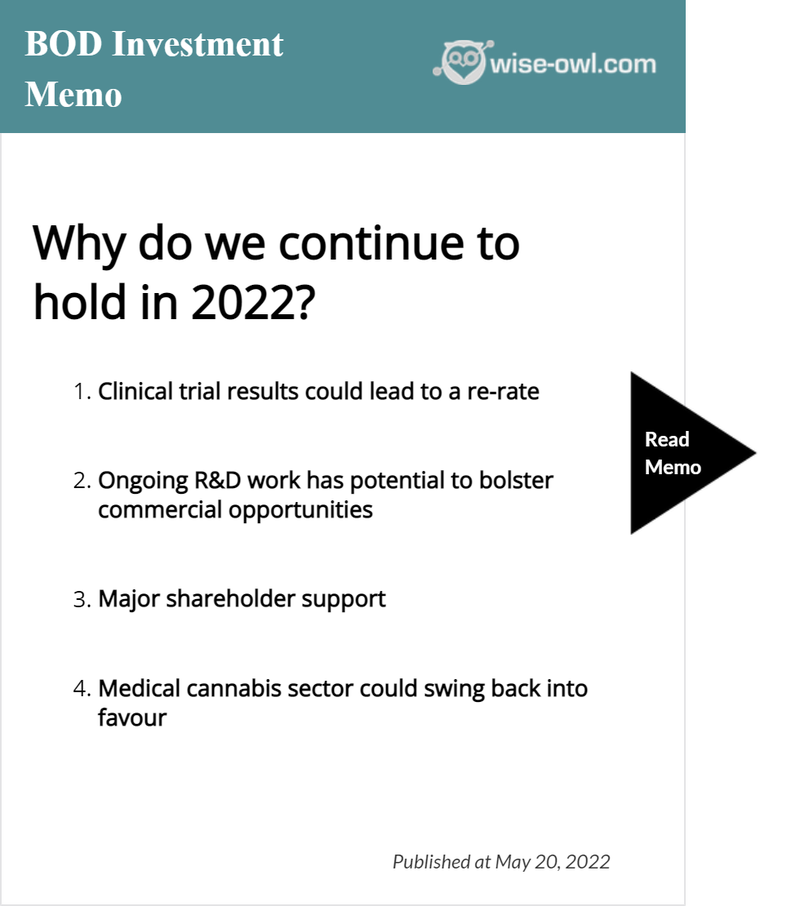

Why do we continue to hold in 2022?

We have four key reasons we continue to hold BOD (click the image to see the full version of these reasons):

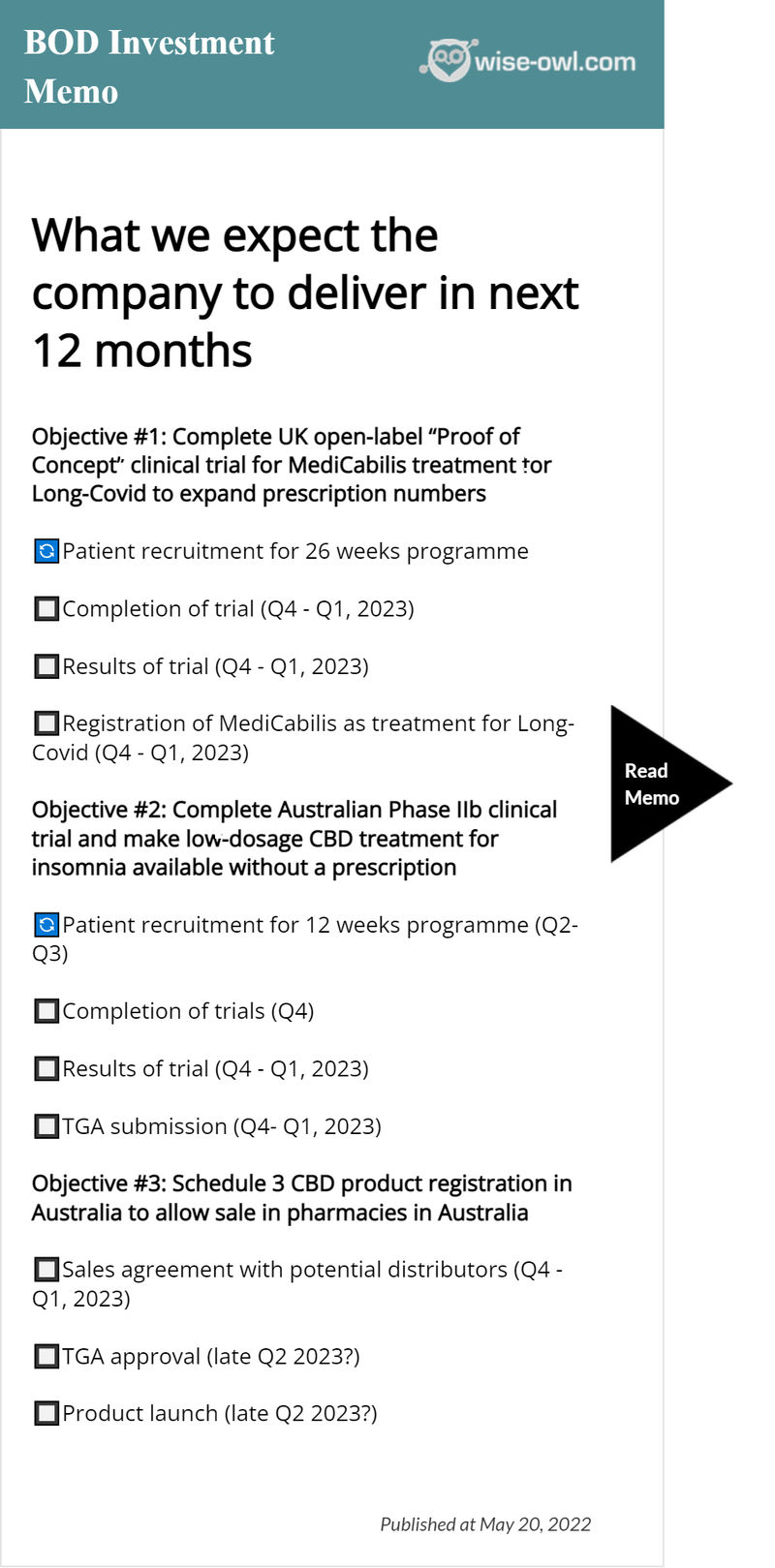

What we expect the company to deliver in 2022

We view 2022 as a significant year for BODs development:

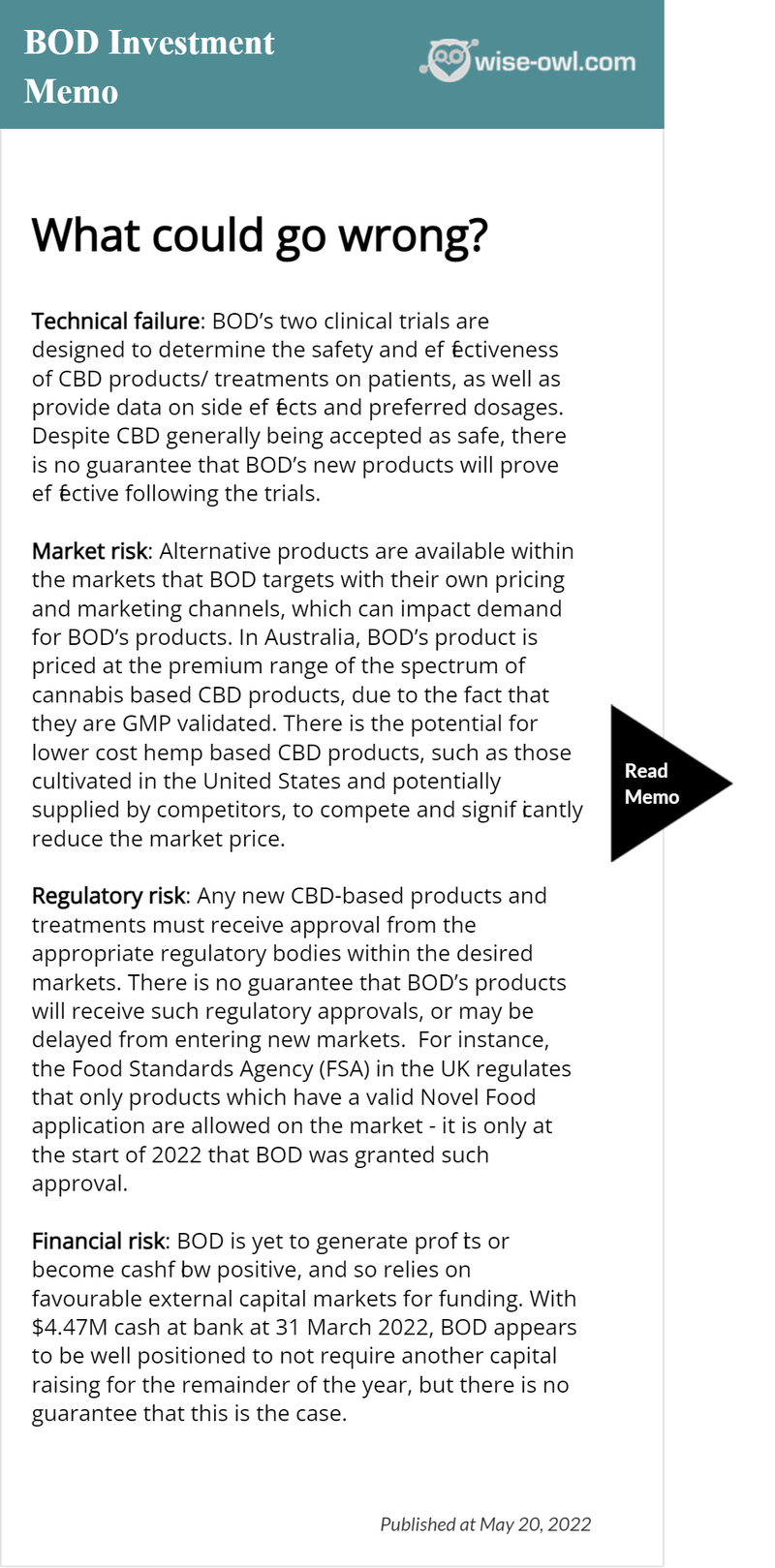

What are the risks

We have identified four risks for BOD:

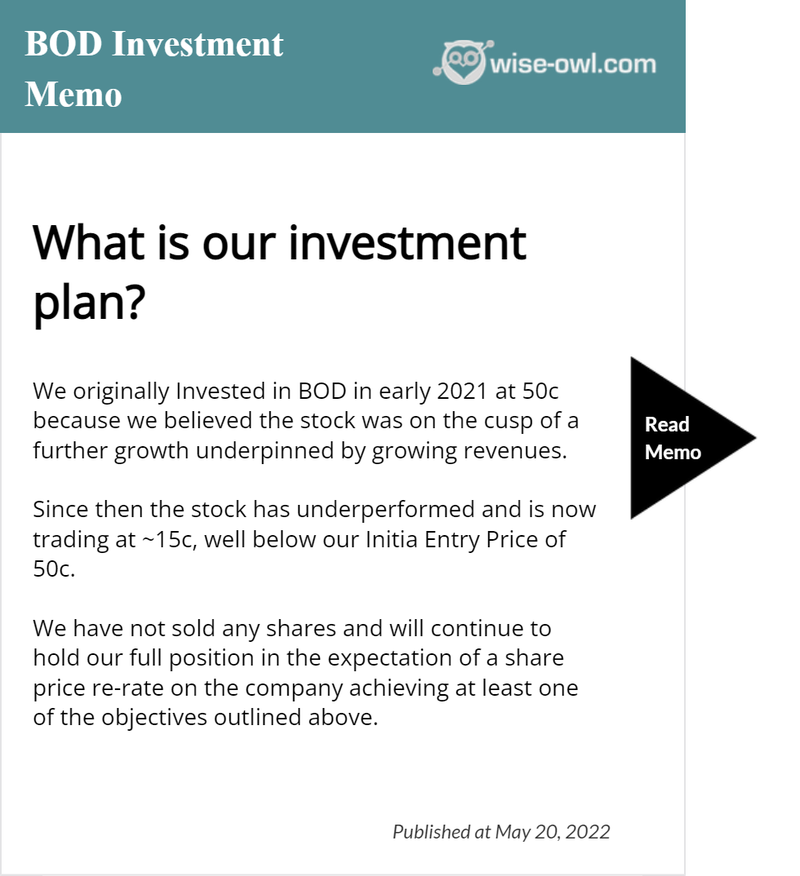

What is our investment plan?

This is how we intend to Invest in BOD:

Conclusion:

We’ll be following BOD’s progress over the next 12 months and want to see success in their clinical trials. To track this progress we’ve now launched our BOD 2022 Investment Memo.

Below is our 2022 investment memo for BOD including:

- Key objectives for BOD in the next 12 months

- Why we continue to hold BOD

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.