Offtake to drive Takeoff

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Overview: Centaurus Metals Ltd ("Centaurus", "the Company") is an Australian minerals company focused on developing iron ore mining operations in Brazil. Ore Reserves totalling 48.5million tonnes (Mt) have been delineated as part of a Bankable Feasibility Study (BFS) at its most advanced Project, Jambreiro. The Company has established a broader mineral Resource portfolio totalling 216Mt, inclusive of Reserves.

![]()

Catalysts: Development of Jambreiro into a producing mine is Centaurus’s major value growth driver. With feasibility and permitting works completely, an offtake partnership and procurement of construction finance would send a strong signal of the asset’s near-term, scalable cash flow potential.

Hurdles: With almost two years passing since completion of the original Jambreiro BFS, marketing and execution risks are impacting confidence toward the stock. Management must contend with international price benchmarks one third lower year to date, and a funding environment contingent on offtake clarity.

Investment View: Centaurus offers speculative exposure to the iron ore mining industry and Brazilian steel demand. We are attracted to the advanced status of its Jambreiro Project, and value growth which pending offtake and funding events could deliver. Whilst they may require a recovery in international price benchmarks, a high degree of risk appears to be factored into the stock. With our valuation offering a premium of 170 percent to recent trade and varying to iron ore prices by a factor of three, we initiate coverage with a ‘speculative buy’ recommendation.

Company Overview

Centaurus Metals Limited ("Centaurus", "the Company") is an Australian minerals company with iron ore assets in Brazil. Its most advanced project is Jambreiro, located in the State of Minas Gerais, which accounts for over 60 percent or 170mtpa of Brazil’s iron ore production. Mineral reserves of 48.5million tonnes (Mt) have been delineated at Jambreiro as part of a Bankable Feasibility Study. The reserve estimate is contained within a mineral resource portfolio totalling 216Mt.

Centaurus Resources Ltd was founded in June 2006 and listed on the Australian Securities Exchange in August 2007 upon raising $4million at 20c/share (CUR.ASX). After procuring a portfolio of Brazilian mineral assets, Centaurus Resources Ltd executed a merger with Glengarry Resources Ltd (GGY.ASX) which closed in February 2010. The scrip based transaction saw shareholders of Centaurus Resources Ltd receive 53 per cent of the merged entity.

Advanced Brazilian Iron Ore Portfolio

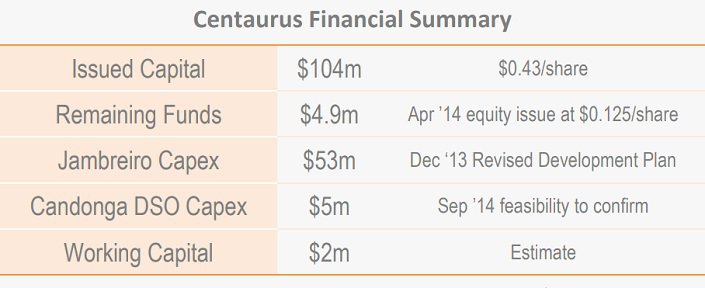

The Company commenced trading as Centaurus Metals Ltd (CTM.ASX) in April 2010. Issued capital currently stands at $103.5million, or $0.43/share.

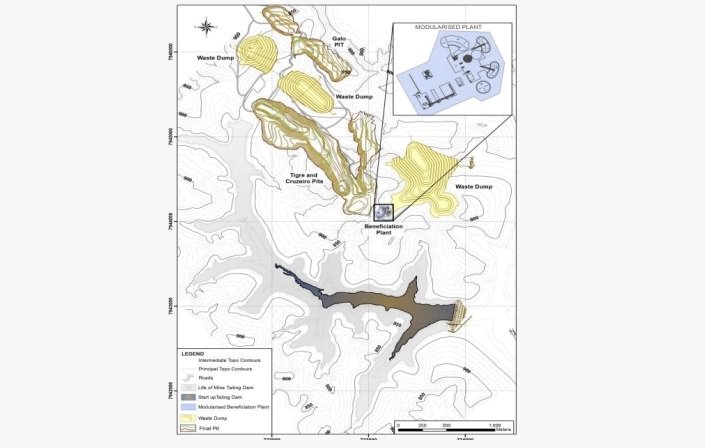

Asset Overview – Jambreiro (100%)

The Jambreiro Iron Ore Project consists of three Mining Leases covering 32.7.km 2 in the State of Minas Gerais, Brazil. The Jambreiro Project site is located approximately 200km northeast of the State Capital, Belo Horizonte, and 12km from the township, São João Evangelista.

The project is located close to existing infrastructure including good quality sealed roads, a sealed airstrip, industrial water supply and high voltage power, all of which are readily available for use by the Company. The steel-making region, Ipatinga is situated 110km south.

Centaurus acquired the Jambreiro Project in June 2010 as part of an 18 tenement package within Minas Gerais for US$3million plus a future production royalty.

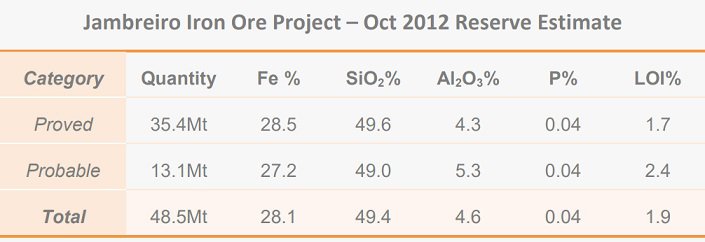

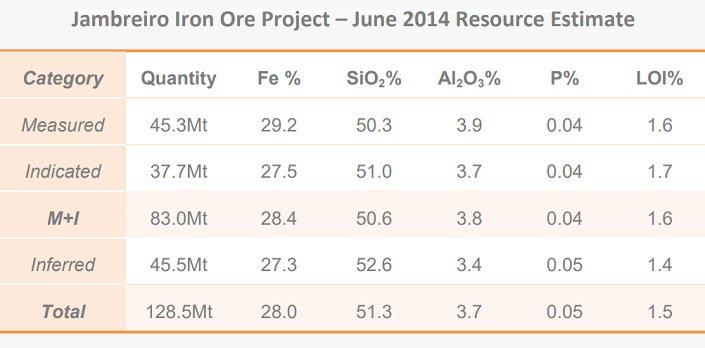

The area under Mining Lease was the subject of a Bankable Feasibility Study (BFS), completed in November 2012. Within the Mining Leases, Measured, Indicated, and Inferred Resources totalling 128.5million tonnes have been delineated, from which Proved and Probable Reserves totalling 48.5million tonnes were established as part of the BFS.

Proved + Probable Reserve 48.5mt

Significantly, the Reserve estimation only incorporated near surface material otherwise known as ‘friable’ ores. Deeper ‘compact’ material which comprises approximately half of the Measured and Indicated Resources were excluded from the Reserve estimation despite satisfying open-pit mining requirements.

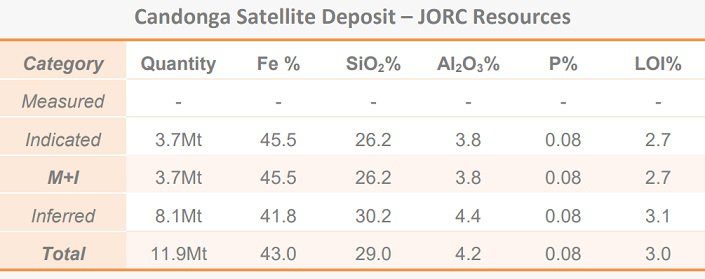

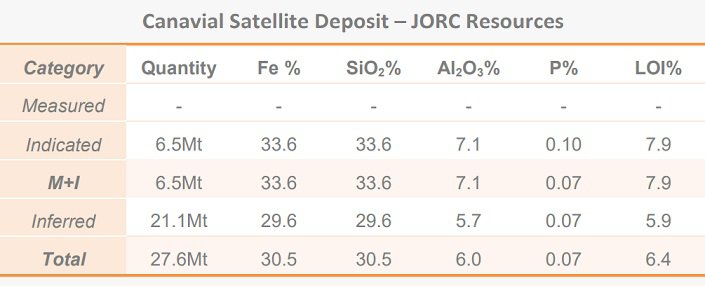

Subsequent to completion of the BFS, Centaurus has outlined additional mineral resources proximal to the Mining Leases within its Canavial and Candonga tenements ("Jambreiro Satellite Deposits"). Indicated and Inferred Resources totalling 39.5Mt have been delineated.

Significantly, the Candonga Resource contains 0.9Mt of Direct Shipping Ore ("DSO") grading 58.6% Fe which is now the focus of additional drilling and feasibility works to support a potential small scale production opportunity.

DSO opportunity at Jambreiro Satellite Deposits

Development Strategy

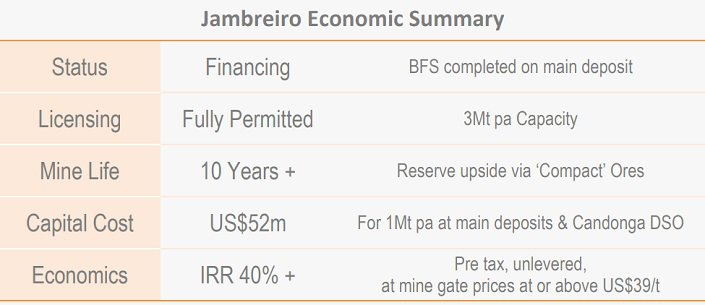

Completed in November 2012, the Jambreiro BFS appraised the economics of a nine year mining and beneficiation operation producing 2Mt pa of high grade (+65% Fe), low impurity sinter blend concentrate for domestic steel markets.Candonga DSO being investigated as an early cash flow opportunity

Whilst development scenario’s considered in the BFS indicated robust economics (post-tax IRR 33%, NPV8 $140million), Centaurus is pursuing a staged development strategy to reduce start-up capital requirements.

The Staged Development Plan was announced in December 2013. It envisages an initial 1Mt pa operation, with the ability to expand. Benefits include large reductions in preproduction capital expenditure, an accelerated development timeline, and greater financing flexibility.

Release of the Staged Development Plan coincided with the receipt of Mining Leases in January 2014. Jambreiro is now fully licensed and permitted to deliver 3Mt pa.

Higher grade ore recently delineated at the Candonga satellite deposit is being investigated as an early stage cash flow opportunity. A decision on its role within the Jambreiro development is expected in Q4 2014 with the first production possible in Q1 2015.

Economics

Completed feasibility works to date have focused on the main Jambreiro deposit. Investigations currently underway for the Candonga satellite deposit could confirm a small-scale but potentially high-value addition to the mine plan.

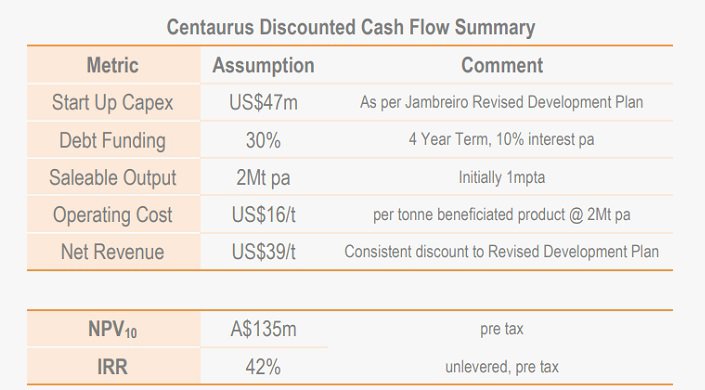

Discussions with management suggest Candonga could be brought into production rapidly for a capital outlay of no more than A$5million. It is envisaged that cash flow generated at Candonga be used to supplement funding for the main Jambreiro deposit, which is expected to require a capital investment of A$53million (US$47million) to establish a 1Mt pa operation.

The difference in capital requirements relates primarily to Candonga’s smaller operating scale and absence of a beneficiation plant, which is needed to treat Jambreiro ores.

Whilst further investigations are required to ascertain Candonga’s operating metrics, Jambreiro, operating cash costs plus royalties are estimated to be A$22 (US$20) per tonne of saleable concentrate at the mine gate.

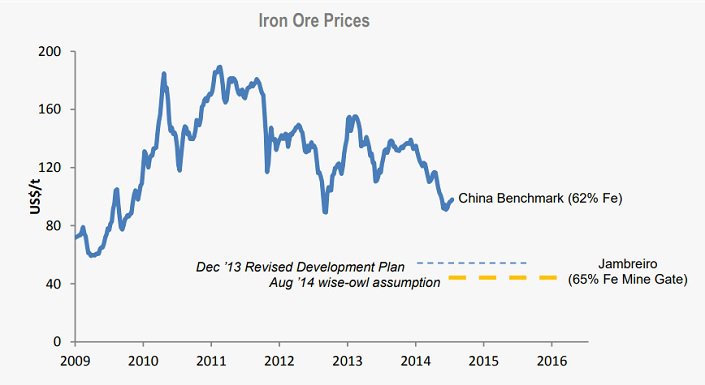

Subsequent logistics charges associated with road transportation to domestic steel mill customers are scheduled to be incorporated into selling prices. Jambreiro concentrate pricing is expected to be referenced to the international CFR China 62% Fe benchmark ("China benchmark"), adjusted for grade and quality characteristics.

Centaurus's staged development plan budgeted an initial mine gate sales price US$53/t (after logistics ‘net backs’), which represented a discount exceeding 55 per cent to the prevailing China benchmark of US$120/t.

Robust economics at net pricing of $39/tonne

The China benchmark has subsequently contracted below US$100/t. Whilst linearity of its relationship with Jambreiro concentrate has yet to be tested, a similar discount would yield a selling price of US$39/t, after logistics netbacks

At this price, our modelling indicates the Jambreiro Project generates an unlevered, pre tax Internal Rate of Return above 40 percent. However, in the absence of an offtake partner, the reference price methodology surrounding Jambreiro remains a major source of risk.

Asset Overview – Itabira Projects (100%)

The Itabira Projects consist of 3 exploration licenses spanning 41km 2 in the State of Minas Gerais, Brazil, approximately 80km northeast of the State Capital, Belo Horizonte. Vale’s 40mtpa Southern System iron ore operations at Itabira are situated within 30km, the State’s largest smelter, Usiminas’ Ipatinga, is located within 80km, and Arcelor Mittals’ steelworks at Joao Monlevade and Timóteo are within 50km.Additional 49mt resource at Itabira Projects

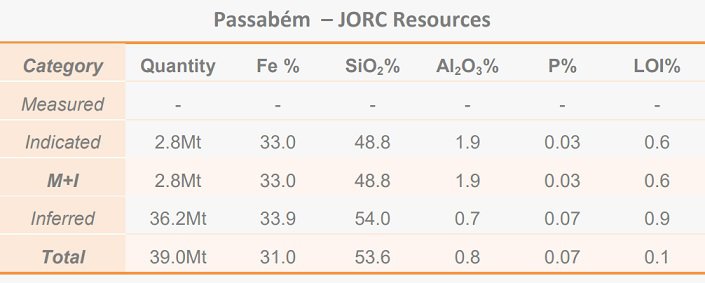

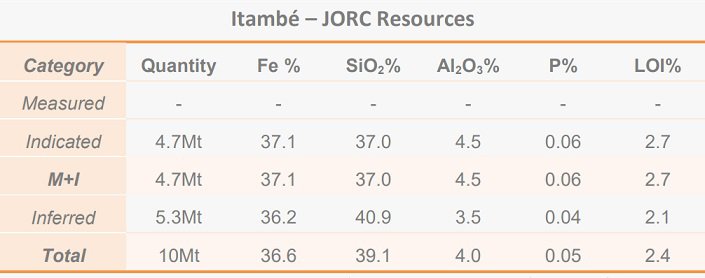

The Itabira Projects were acquired by Centaurus Resources Ltd in April 2008. The Company has subsequently delineated Indicated and Inferred resources totalling 49million tonnes at the Itambé and Passabém project sites. A scoping study on the Itambé project area was completed in August 2009.

Development Strategy

The Itambé scoping study appraised a staged DSO development initially producing 0.5Mt pa for domestic steel markets. The Passabém and Itambé mineral resource estimates were updated in late 2010. Concurrent metallurgical testing indicated the deposits are more suitable for a beneficiated development, similar to that being pursued at Jambreiro. Whilst further feasibility studies are required to establish the merits of such a development, Centaurus is presently prioritising capital towards Jambreiro.

Financial Performance

As its mineral assets are still in the development phase, Centaurus is reliant on external capital to advance their development. To date, the Company has funded activities through equity.~$60million capital requirement for Jambreiro

Issued capital currently stands at $103.5million, or $0.43/share. The Company’s last equity issue concluded in May 2014. $5.5million was raised at $0.125/share, resulting in the issue 44.2million shares, expanding total shares outstanding by 22 per cent. To establish production at Jambreiro, we estimate the Company will require additional capital of at least $60million. Management is considering debt and equity financing structures.

Valuation

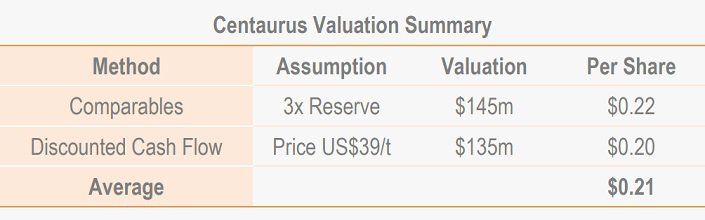

Centaurus’s investment appeal rests in the development potential of its iron ore portfolio. We have focused our appraisal on its Jambreiro Project, utilising a Comparables-based approach and Discounted Cash Flow methodology.

Per-share valuations are derived from both methods by assuming pre production capital is funded 30 per cent debt with the balance equity at $0.10/share.

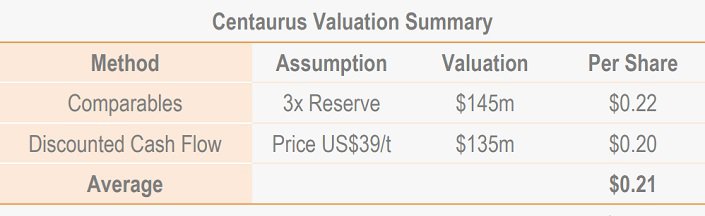

Valuation $0.21/share

The Discounted Cash Flow arrives at a valuation of $135million which equates to $0.20/share. Our Comparables approach arrives at a valuation of $145million, which equates to $0.22/share. Applying equal weightings both methods deliver an aggregate valuation of $140million or $0.21/share.

Comparables

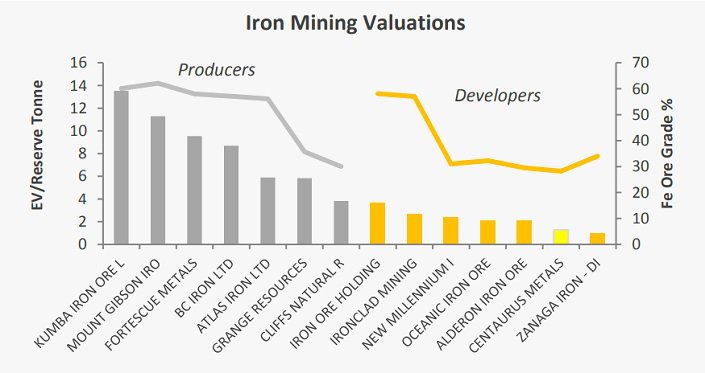

Our peer-based valuation of Centaurus is based on a universe of publicly listed companies with predominantly iron ore mining assets. The average valuation for existing producers is presently above $8 per tonne of Reserve. The average valuation for companies with assets in the development phase is presently above $2 per tonne of Reserve.Reserve multiples suggest a transition to ‘Producer’ status offers significant value growth

Developer valuations include forecast capital expenditures. Adjustments have been made for Companies with non-controlling interests, whilst non-producing assets without assigned capital expenditure have been omitted.

Centaurus is presently in the development phase. Its current Reserve multiple of ~$1.30 per tonne stands at the lower end of the Developer peer group. After procuring project finance and commencing sales, the present valuation curve suggests a higher multiple is possible.

The Producer group average Reserve multiple is above $8 per tonne. Considering the grade characteristics of Jambreiro ore, we believe a multiple toward the lower end of the Producer range is an appropriate target.

Comparables based valuation $0.22/share

Applying a $3 per tonne Reserve multiple offers a target Enterprise Value of $145million, post capital investment. Assuming equity proceeds are procured at Centaurus’s volume-weighted average price of $0.10/share, the Comparables valuation equates to $0.22/share.Discounted Cash Flow

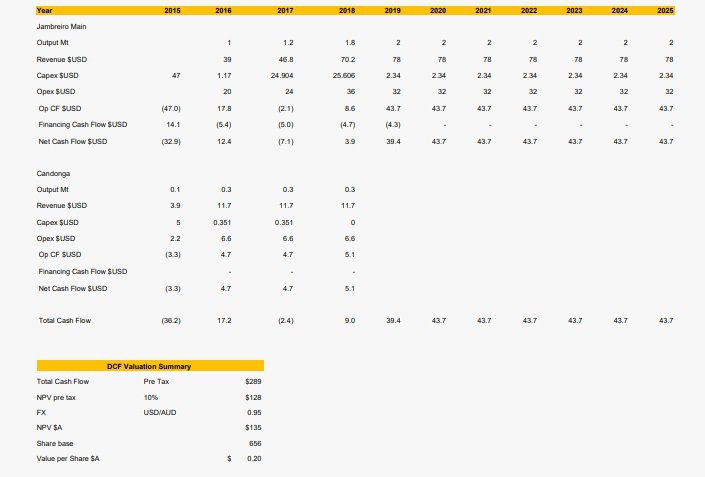

Incorporating the December 2013 Staged Development Plan, we have modelled a ten-year operation at Jambreiro initially producing 1million tonnes pa.

A staged expansion to 2Mt is forecast, funded by cash flow from a concurrent DSO operation at Candonga. We’ve assumed Candonga delivers 1Mt over a three to four-year period.

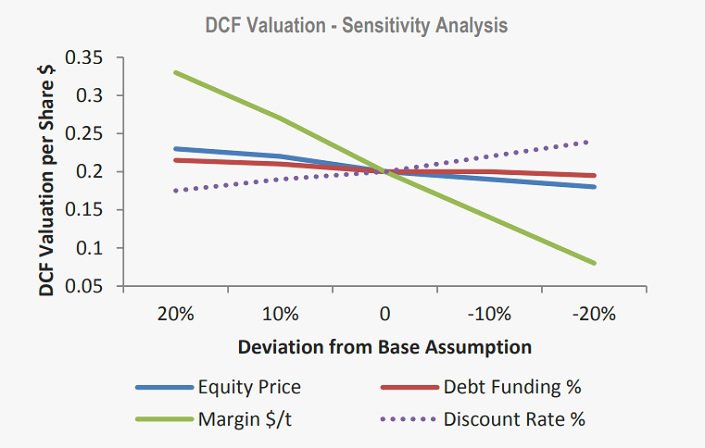

Utilising US$39 per tonne as a base case pricing scenario for Jambreiro product, applying a 10 per cent discount rate, and 30 per cent debt funding to its initial capital requirement, we calculate a pre tax Net Present Value of A$135million.

DCF Valuation $0.20/share

Assuming equity proceeds are procured at $0.10, the Discounted Cash Flow valuation equates to $0.20/share.

Investment View

Centaurus offers speculative exposure to the iron mining industry and Brazilian steel demand. We are attracted to the advanced status of its Jambreiro Project, where feasibility works have been completed to a Bankable level, and near-term cash flow opportunity provided at Candonga.

Development of Jambreiro into a producing mine is the Company’s major value growth driver. Valuation multiples ascribed to existing iron ore producers are at least double those attributed to developers. This compliments our aggregated valuation of Centaurus representing a premium of 170 percent to recent trading levels.

Valuation represents 170 percent premium to recent trade

However, with almost two years passing since completion of the original Jambreiro BFS, marketing and execution risks are impacting confidence toward the stock. Management must contend with international price benchmarks one third lower year to date, and a funding environment contingent on offtake clarity.

Delivery of an offtake partner and subsequent funding are the major near-term catalysts for Centaurus. Whilst they may require a recovery in international price benchmarks, a high degree of risk appears factored in to the stock price.

Three-fold valuation leverage to iron ore price

Changes to our base case revenue assumption impact Centaurus’s valuation by a factor of three. As Jambreiro presents a ‘turn-key’ opportunity to capture favourable market conditions, we initiate coverage with a ‘speculative buy’.

Risks

Technical Risks

Whilst economic studies at Jambreiro have been conducted to a BFS level, there is no guarantee that actual mining and processing results will meet operating and capital cost forecasts. Feasibility studies are ongoing at Candonga, creating uncertainty surrounding its possible contribution to forecast expansions at JambrieroMarket Risks

Although the state of Minas Gerias hosts a significant steel-making industry, and offtake discussions are underway, there is no guarantee Centaurus will be successful in marketing its planned 1mtpa production from Jambreiro. There is also a risk that revenue per tonne is lower than scheduled as pricing will be linked to international spot markets. The CFR China 62% Fe benchmark has contracted over 20 per cent from its 2013 peak, and there is no guarantee against further declines.Funding Risks

Centaurus is reliant on external funds to sustain operations and requires capital investment in the order of $60million to develop Jambreiro into production. There is no guarantee the Company will be successful in procuring these funds. There is also a risk that future fundraising initiatives generate greater dilution than forecast in our analysis, which would negatively impact our valuation.Scheduling Risks

Delays in project execution, expansion, and financing could impair Centaurus’s valuation to present equity holders. Our Discounted Cash Flow valuation is sensitive to production forecasts, which anticipates sales from Candonga DSO in early 2015 and commissioning at Jambreiro main deposits during late 2015.

The Bulls & The Bears

The Bulls Say

- Jambreiro offers near term development potential, is fully permitted and supported by a Bankable Feasibility Study

- Project development is supported by Internal Rates of Return exceeding 40 percent at net prices at or above US$39/t

- Looming offtake and project financing offer major value catalysts

- Our base case valuation represents a significant premium to current trading levels

The Bears Say

- Revision of Jambreiro from a 2Mt pa operation in the BFS to a 1Mt pa operation has impacted confidence in its development schedule

- Iron ore prices have contracted 30 percent year to date and further declines could significantly impair project economics at Jambreiro

- Absence of offtake agreement impairs confidence in local demand for Jambreiro concentrate

- There is no guarantee the Company will secure the necessary project finance required to bring Jambreiro into production

Management

Didier Murcia – Non Executive Chairman

Mr. Murcia is a lawyer with over 25 years of legal and corporate experience in the resources industry. He currently holds an Order of Australia and is currently Honorary Australian Consul for the United Republic of Tanzania. He is the Chairman and founding director of Perth-based legal group Murcia Pestell Hillard, and is Director at Gryphon Minerals Ltd, Cradle Resources Ltd, & Alicanto Minerals Ltd.Darren Gordon – Managing Director

Mr Gordon is a Chartered Accountant with 20 years’ professional experience, predominantly in the mining industry as a senior finance and resources executive. Mr. Gordon has had extensive involvement in financing resource projects from both a debt and equity perspective, including his previous position as Chief Financial Officer and Company Secretary for Gindalbie Metals LimitedPeter Freund – Non Executive Director

Mr Freund joined Centaurus in 2009, bringing significant experience in progressing major projects from exploration through to production. Prior to coming to Centaurus, Mr. Freund was the General Manager of the Karara Joint Venture between Gindalbie Metals and Ansteel. He also worked for BHP at the Whyalla steelworks and iron ore pellet plant in South Australia, BHP Minerals Division in Melbourne, and the Groote Eylandt manganese mine in the Northern Territory. In South America, Mr. Freund has led the MIM team that constructed the world- scale Alumbrera copper mineMark Hancock – Non Executive Director

Mark is a Chartered Accountant with more than 25 years of professional experience, including senior financial roles across a number of leading Australian and international companies including Lend Lease Corporation Ltd, Woodside Petroleum Ltd, and Premier Oil plc. Since 2006 he has held senior roles at Atlas Iron Ltd, most recently as Chief Commercial Officer. Over that period Atlas has grown from a junior explorer to fast growing producer and member of the ASX 100. In addition Mark has served as Atlas’ representative on the Board of other ASX listed iron ore players, Warwick Resources, Aurox Resources and Giralia Resources.John Westdorp – Chief Financial Officer

Mr. Westdorp is a Chartered Accountant with 20 years of resource experience. He is former CFO of Iron Ore Producer, Murchison Metals. He has held senior positions with North Ltd Group including 6 years with Robe River Iron Associate JV.

Appendix - Discounted Cash Flow

Notes

1. All figures in USD millions unless stated otherwise

2. Net Present Value and per share Value is pre-tax

3. All salable output is presently categorized as Reserve, except Candonga material, which is Indicated (0.7Mt) Inferred (0.2Mt)

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.