Time to Subscribe as Collaborate Gains Momentum

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Overview: Collaborate Corporation Ltd ("Collaborate", "CL8", "the Company") is an Australian technology company providing mobility solutions to the automotive industry. Collaborate allows automotive manufacturers and dealers to access new revenue streams for vehicles through its operation of online marketplaces. The Company's primary focus is DriveMyCar (peer-to-peer car rental) and Carly (car subscription). Wise-owl first initiated coverage in April 2017 and our last update was a ‘speculative buy’ recommendation in October 2019.

![]()

Catalysts: Collaborate is on track to deliver improved financial performance, delivering four consecutive quarters of growth and realising significant cost savings. Continuation of this trend could be a major value driver as the year progresses. The coming launch of Carly in New Zealand could add to recent momentum, while a gradual expansion of the Carly ecosystem has the potential to deliver revenues and attract additional strategic partners. Recent capital raisings, including two strategic investments from key industry players, mitigate funding risks and validate Carly’s value proposition.

Hurdles: While no more capital will be required in the near-term, Collaborate remains reliant on external capital and there is no guarantee that future funding can be procured at favourable terms to shareholders. Collaborate has a first-mover advantage in targeting the growing car subscription industry, however, the Company may be subject to the increasing competition which could put pressure on future pricing power. While early data indicate a sound commercial model, the long-term viability of Carly remains to be validated.

Investment View: Collaborate offers speculative exposure to the emerging car subscription industry. Following the successful launch of Carly, Collaborate is well-positioned to take advantage of the significant growth opportunity in the car subscription market in the ANZ region with a first-mover advantage. Recent funding via strategic investments, entitlement issue and option exercise mitigates near term funding demand as the Company builds toward a critical mass. The company experienced growth across key metrics during the past four consecutive quarters and appears to have all systems in place to resume this trend in a capital-light business model. Principal hurdles include the Company’s need to reach a self-funding position and the risk of increasing competition. With management demonstrating their ability to forge and leverage corporate partnerships, and Carly demonstrating early traction, we anticipate the recent uptrend to continue to deliver a gradual re-rating in the stock as Collaborate’s mobility solutions witness benefits of scale. We resume coverage with a ‘speculative buy’ recommendation.

COMPANY OVERVIEW

Collaborate Corporation provides mobility solutions to the automotive industry allowing automotive manufacturers and dealers to access new revenue streams for vehicles

Collaborate’s key online marketplaces include.:

- DriveMyCar (peer-to-peer car rental)

- Carly (car subscription)

Each asset leverages Collaborate’s expansive ecosystem of partnerships and as is designed to create ‘trust’ for individuals and companies to transact with each other for mutual benefit.

CL8’s share price has risen ~100% since the September low

Collaborate operates in the collaborative economy or sharing economy and is listed on the Australian Securities Exchange (ASX) with the ticker code CL8. At the date of this report Collaborate had a market capitalisation of $16.1 million and was last traded at $0.014 per share.

ASSET OVERVIEW

Collaborate’s most advanced assets is DriveMyCar , a peer-to-peer marketplace that allows car owners to rent vehicles to third parties. DriveMyCar is tailored for both private and corporate clients. DriveMyCar was founded in 2010 and acquired by Collaborate in 2014.

The platform was initially designed for private consumers, however, Collaborate’s strategic focus on corporate partnerships has allowed car dealers, manufacturers and other fleet owners to monetise assets through Collaborate’s online marketplace. The DriveMyCar marketplace has over 600 active vehicles as of July 2019.

Carly , a vehicle subscription service, which was launched in March 2019, leverages the technology, capabilities and fleet supply partners of DriveMyCar. Carly allows consumers to access a range of new and used vehicles including insurance, registration and maintenance packaged into a monthly payment.

Carly vehicle subscription is an alternative to buying a car or committing to a loan or lease. Subscriptions can be paused if not required and vehicles can be switched instantly if desired without any long-term commitments. Carly is currently available in Sydney and Melbourne and a launch in New Zealand is expected in March 2020.

Across all marketplaces, Collaborate has delivered over 400,000 rental days, paid over $10 million to vehicle owners and has over 60,000 registered users.

The PeerPass Platform underpins both assets and was developed by Collaborate to verify customers and perform credit checks to improve effectiveness and deliver a lower Insurance Claims Loss Ratio than the industry average.

MARKET OVERVIEW

The recently launched car subscription service Carly taps into the growing demand for flexible access instead of ownership.

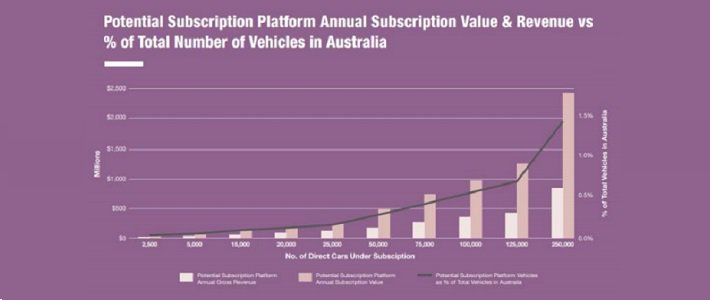

Car subscription opportunity could be worth $100 billion in 2025

According to Deloitte's 2019 Global Automotive Consumer Study, an increasing number of millennials are questioning the need to own a vehicle. In developed markets between 33% and 60% of Gen Y/Z ride-hail users favour shared mobility solutions.

As consumers look for more flexible ways to access vehicles and consumers increasingly see ownership as a burden, there is potential for Carly to "disrupt" the traditional car sales market., which has seen little innovation to date in Australia.

Combined, Carly and DriveMyCar, provide an alternative solution to the car sales and rental markets

The domestic car rental market is estimated at $3 billion per annum and is currently dominated by conventional short term rental agencies which typically own their own vehicle fleet. Peer-to-peer rentals currently represent a small yet fast-growing segment.

Based on Vfacts annual sales data and NSW Government information, the annual value of car sales in Australia is estimated to be $60 billion per annum with over 3 million units sold each year. The industry is experiencing headwinds, with data from the Australian Automotive Industry showing declines year-on-year for new car sales.

Regulatory challenges could further challenge the industry on the back of a launched investigation into the $8 billion motor vehicle finance industry by the Australian Securities and Investments Commission in mid-2018. Regulatory tightening and a shift in consumer preferences have created an industry that is ripe for disruption. New car sales are declining, dealer profit margins are challenged and access to finance for car buyers is expected to tighten. The recent trend suggests that loan application rejection rates could further increase, which has the potential to drive demand for alternative providers such as Carly, which does not require consumers to enter into long term financial agreements.

While the Australian car subscription market is still in its infancy with virtually no established competitors. Developed markets in Europe and North America have seen rapid adoption of vehicle subscription. Providers include Original Equipment Manufacturers (OEMs), mobility providers, dealers and technology startups.

Frost & Sullivan estimates that by 2025-26, vehicle subscription programs could account for nearly 10% of all new vehicle sales in the US and Europe, predicting a real market opportunity worth almost US$100 billion a year.

DEVELOPMENT STRATEGY

Since launching the Carly service in Q1 2019, the Company has focused on scaling the service via strategic partnership and geographic expansion. As Collaborate has built a network of automotive partnerships through its DriveMyCar business, Carly benefits from a wide range of existing strategic partners.

Carly has attracted major supply deals with established brands

Carly launched in Sydney in March 2019 with 130 vehicles from 13 brands featuring 30 models. Collaborate has expanded the Carly offering to Melbourne and is expected to launch in New Zealand in March 2020, in partnership with Turners Automotive,

Vehicles available for booking are supplied by third-party providers, including automotive dealers, manufacturers, corporate fleets and private car owners. There are no upfront costs associated with the procurement of the fleet as Collaborate does not own the inventory.

Combined, Carly and DriveMyCar, provide an alternative solution to the car sales and rental markets

Carly has attracted a number of potentially significant partners since launch, including;

- Turners Automotive Group (ASX:TRA), the largest seller of cars in New Zealand with a market capitalisation of ~$230 million (as of January 2020).

- Hyundai, the third largest automotive vehicle manufacturer by volume in Australia, with a nationwide network of 172 dealerships

- Suttons Motors, an NSW dealership group with access to 27 franchised dealerships located primarily in Sydney

- SG Fleet Group Limited (ASX:SGF) with a presence across Australia, the UK and New Zealand with approximately 140,000 vehicles under management

- i-Motor offers a potentially compelling, scalable solution that enables consumers to subscribe to cars directly from dealer

Carly leverages the existing technology and footprint from the DriveMyCar business, which will allow Collaborate to mobilise complementarities and exploit cost and operational synergies of the two business units.

The Company’s verification platform PeerPass provides Collaborate with a competitive advantage by reducing risk and encouraging growth in the supply of assets and creating a pool of verified customers. PeerPass adds the ‘trust’ component to Collaborate’s platforms by verifying customers in real-time before they gain access to a vehicle.

Collaborate is expected to continue to direct its resources towards its mobility strategy in the car rental and car subscription market. The Company announced on 30 January 2020 that operations of the Mobilise platform will cease and that the future focus for the MyCaravan business is under review. The refined strategy will allow Collaborate to focus on DriveMyCar and Carly.

ECONOMICS

Collaborate has created a marketplace for users to exchange goods and revenue is derived from the total value of goods offered across all platforms and users’ willingness to make bookings.

Average revenues of $303 per month & vehicle with potential for growth

Collaborate generates revenue when a customer makes a booking on one of its online marketplaces – Carly or DriveMyCar. The value of the transaction is typically correlated to the market value of the asset and the duration of the confirmed booking. In addition, Carly generates income from a platform licence fee based on subscription revenue, custom technology development and the provision of customer service.

Collaborate retains a commission whilst paying back a portion of the fee to the owner of the asset.

Based on the most recent subscriptions, the average total subscription value totalled $863 per month per vehicle (ex GST) and the average Carly revenue was 35% or $303 per month per vehicle (ex GST). The current average gross margin equates to 36% after insurance and other variable costs. Collaborate sees potential to deliver an increased average gross margin of up to 60% from variable cost savings due to economies of scale.

Carly experiences 36% RTV growth in December quarter

Early data suggest that Carly can be scaled in a capital-light business model via channel partnerships. The model is dependent upon the supply of vehicles by strategic partners and the uptake of the subscription service by consumers.

Receipts from customers increased by 20% in the December 2019 quarter, the fourth consecutive quarter of growth as Carly experiences growth across key metrics. Carly Rental Transaction Value (RTV) increased by 36% quarter-on-quarter.

Whilst supply on the platform has historically been a limiting factor, discussions with commercial partners are positioning the Company to accelerate uptake.

Source: Collaborate Investor Presentation July 2019

FINANCIAL PERFORMANCE

Collaborate currently generates revenue from transactions across its online marketplaces Carly and DriveMyCar. The Company charges rates based on the market value of rentable assets and generates gross revenue by charging administration and insurance fees. Cash flow is a result of the total rental transaction value, thus significantly higher than gross revenue.

[callout class="center_callout" layout="layout_one" title="59% increase in gross profit in Q4 vs pcp" imgsrc="https://wise-owl.com/uploads/2021/01/Graph-Icon_1.jpg"][/callout]

Over the past year, Collaborate has increased its focus towards its mobility strategy and implemented strategic cost initiatives delivering an improved financial performance. Collaborate experienced its fourth consecutive quarter of growth during the December 2019 quarter.

Gross profit increased by 59% on the previous corresponding period as a result of broad growth in Rental transaction Values (+20% on pcp) and a significant reduction in corporate and administration costs (-44% quarter on quarter).

Carly delivered a 36% increase in RTV, evolving into one of the key drivers of the business, albeit coming off a low base.

To date, the Company has funded operations via equity and debt and most recently raised a total of $2.24 million of funding from a strategic investment by the SG Fleet Group and the exercise of employee options. The placement shares were issued in two tranches at an average price of

$0.014 cents per share.

The proceeds will be used to fund demand generating marketing initiatives and to pursue business development opportunities to grow the available fleet size.

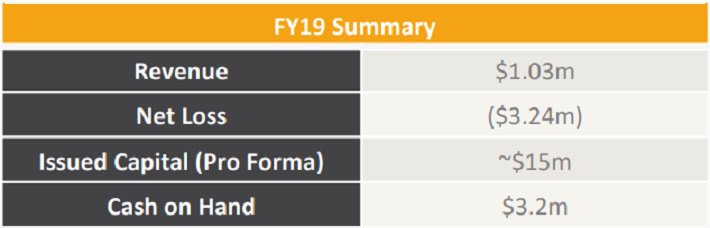

Following the acquisition of the DriveMyCar IP and subsequent change of business direction, we estimate issued capital relating to the existing business to stand at ~$15 million.

INVESTMENT VIEW

Collaborate offers speculative exposure to demand for mobility solutions to the automotive industry.

Carly has a first-mover advantage in the Australian vehicle subscription market and its launch was well received by the local industry, attracting a number of high-quality strategic partners and investors in its first year of operation.

As industry demand is forecast to grow, management’s ability to extract value from these partnerships could be a major value driver and deliver a step-change in revenues for Collaborate.

Wise-owl retains speculative buy recommendation

Following a period of "lumpy" revenues, Collaborate has delivered four consecutive quarters of growth and continuation of this trend – primarily driven by the Carly business – could be a major value driver.

The upcoming launch of Carly in New Zealand could further add to recent momentum while a gradual expansion of the Carly ecosystem has the potential to attract additional strategic partners.

Principal hurdles include the Company’s need to reach a self-funding position and the risk of increasing competition. Recent funding via strategic investments, entitlement issue and option exercise mitigates near term funding risks as the Company builds toward a critical mass.

With management demonstrating their ability to forge and leverage corporate partnerships, and Carly demonstrating early traction, we anticipate the recent uptrend to continue to deliver a gradual re-rating in the stock as Collaborate’s mobility solutions witness benefits of scale.

We resume coverage with a ‘speculative buy’ recommendation.

RISKS

Technical Risk

Critical to the sustainability of Collaborate’s business strategy is the Company’s ability to deliver continued growth in the Carly and DriveMyCar businesses. DriveMyCar has established revenue streams in a developed market and there is no guarantee that Carly will follow the same trajectory.Competitive Risk

Whilst corporate partnerships and the integrated ID verification platform PeerPass provide Collaborate with a competitive advantage, entry barriers surrounding Collaborate’s assets are limited to ‘know how’, speed to market, and its ability to establish a critical mass. There is a risk that its mobility platforms become subject to the increasing competition which may mitigate Collaborate’s competitive edge.Market Risk

To stimulate demand, the cost and convenience of its services need to be attractive versus alternatives such as purchasing or renting from a conventional vendor. There is no guarantee that Collaborate can maintain a favourable price and convenience arbitrage over such alternatives. The vehicle rental and insurance market are highly regulated. Collaborate’s PeerPass platform mitigates the Company from adverse regulatory shifts, however, there is no guarantee its business model is fully insulated from such changes.Funding Risk

Whilst Collaborate generates revenue from transactions across its platforms, income has yet to reach sufficient levels to reduce its reliance on external capital. While the Company has been to date able to secure funding arrangements, there is no guarantee that capital resources currently available to the Company will be sufficient for it to reach a self-funding position, or that additional capital would be available if required.THE BULLS AND THE BEARS

THE BULLS SAY

- Collaborate delivers a fourth consecutive quarter of growth, delivers significant cost savings and gross profit growth. Continuation of this trend could be a major value driver

- The upcoming launch of Carly in New Zealand could further add to recent momentum while a gradual expansion of the Carly ecosystem has the potential to attract additional strategic

- Favourable industry and consumer trends are expected to drive demand for Carly, which aims to disrupt the $60 billion car sales market

- Recent funding via strategic investments, entitlement issue and option exercise mitigates near term funding risks as the Company builds toward a critical

- Recent partnerships announced with Hyundai, Turners Automotive, SG Fleet and I-Motor indicates that Carly has a compelling offering in the market.

- Carly represents a strategic expansion of the Company's presence in the automotive mobility sector and significantly leverages the backend technology, platform and resources that exist within the DriveMyCar business. Favourable industry dynamics are expected to drive demand for

THE BEARS SAY

- The success of Carly is dependent on the uptake of the subscription service by consumers, which cannot be predicted accurately at this stage

- While Collaborate is presently well capitsalised, over the long-term there is a need to become self-funding which is not guaranteed

- Collaborate may be subject to increasing competition

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.