FOD is an Emerging Turnaround Story in the Food and Beverage Sector

Company Overview

The Food Revolution Group Limited (ASX: FOD) , specialises in the development of innovative health-focused products that are sold through numerous retail channels in Australia, with an overseas market expansion imminent.

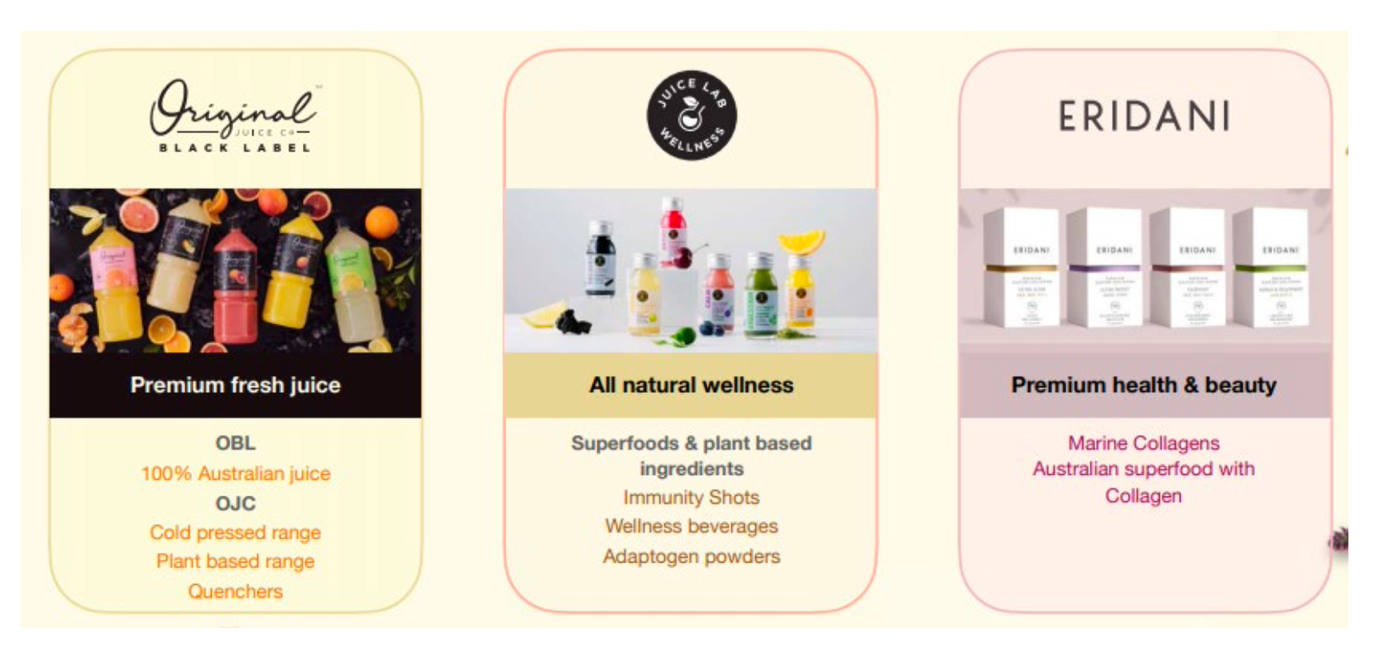

FOD strives to be a leading provider of beverages, functional foods, nutraceuticals, and wellness supplements that improve the quality of consumers lives in the use of all-natural ingredients. Its product range can be seen below:

FOD's recent financials are impressive.

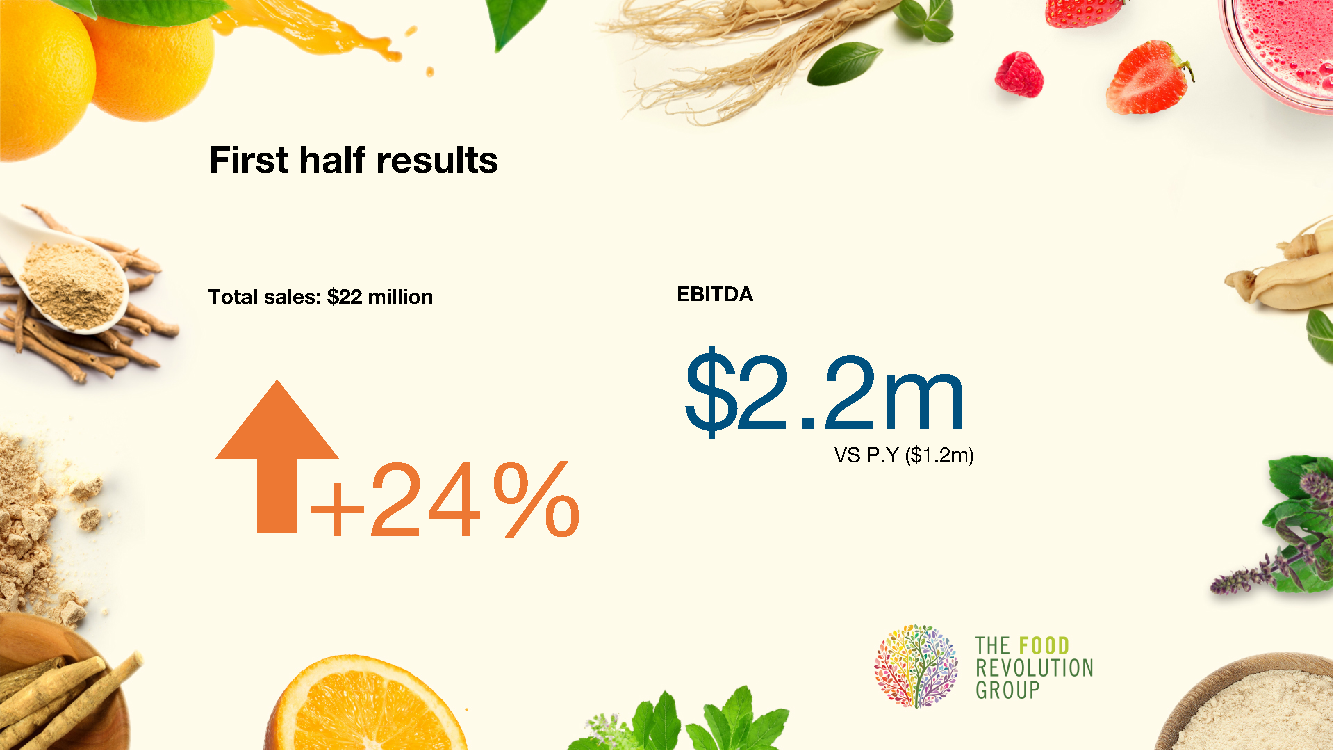

In the six month period to December 31st 2020, the company’s total sales were up 24% to hit $22.2M, delivering $2.2M EBITDA.

The re-branded Original Juice Black Label (OBL) products continue to grow market share with a growth of 18% over the period. OBL continues to outperform the broader fresh juice market, and the brand has increased FOD’s share to 13% of this $560M market.

New products accounted for $1.5M in additional sales.

The gross profit reached $5.69M which equates to 31% of Net Sales.

This turnaround in financial performance reflects improved trading conditions, increasing sales volumes and operational efficiencies.FOD’s goods are sold to all major Australian retailers across Coles, Woolworths, Metcash, IGA, COSTCO and ALDI.

The business is also major contract packers for the retailers’ House brands.

Just recently, FOD was first to market with a plant-based all natural range of products into the $650M Australian wellness category, launching its range of "Juice Lab Super Shots" – the first three variants are now selling in Coles.

We expect this new product range to contribute further to an increase in total sales and revenues, on top of what the company is already delivering.

FOD’s roll-out of wellness products follows a US trend, where the uptake of ‘all natural, pick- me up shots and tonics' has grown substantially on the back of the impacts of COVID-19.

The Foods & Beverages market related to wellness products (preventative) is the fastest growing sector within the $4.8BN US market. The global wellness market is worth US$4.5TN and growing.

FOD is a turn-around story with momentum

The acquisition of the Original Juice Company brand in September 2019, an iconic Australian Brand, was the beginning of FOD’s re-emergence as a powerful Australian retail name.

Through the leadership of CEO Tony Rowlinson, FOD has enjoyed dramatic profitable growth this financial year.

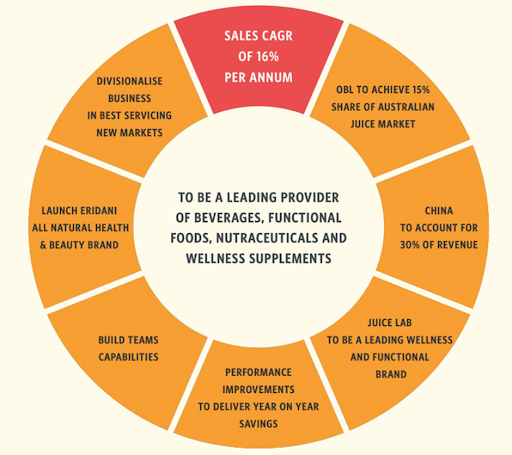

Rowlinson has been busy with the implementation of strategy and the company’s growth plans, while also building the team’s capabilities.

Rowlinson’s goal for FOD is ...

"To be a leading provider of beverages, nutraceuticals, functional foods and wellness supplements, that improve the quality of consumers lives, by the use of all natural ingredients "

The Original Juice Co Brand has been a household staple for over 30 years, and the relaunch of the brand, along with extending the range into functional juices, represents a quantum leap for the company and a vehicle for substantial growth in the near to medium-term.

FOD raised capital of $4.5M in 2020 at 3.5 cents. This price represented a 16 per cent discount to FOD's closing price of 4.2 cents on November 30. FOD is currently sitting at 2.9 cents and a $25M market cap.

We like FOD's valuable asset base. At current levels, given the great turn around, we think FOD seems a prime candidate for a takeover.We have waited for FOD to deliver its first financials under Rowlinson’s leadership and we have chosen now to make an investment.

This is especially the case if you compare FOD to its peers such as the much larger capped Maggie Beer Holdings whose EBITDA is far lower than FOD and in arguably lower growth categories compared to Health and Wellness category.

For these reasons, we think FOD should be trading at multiples higher than it currently is.

Here are some more key reasons we have invested:

- Increased prices of flagship juice

- Reduced costs - negotiated fruit supply agreements

- Processing facility improvements

- New brands

- Launched new strategies

With an impressive year-to-date turnaround in revenue and earnings having been achieved in the December half of 2021, the company is now well-positioned to grow through increased sales and product diversification, which should positively impact the share price moving forward.

Industry and macro drivers

A shift to healthy eating and consumption of more natural products is a key consumer trend that should work in FOD’s favour.

While the short-term impact of COVID-19 was negative for FOD, the long-term implications are extremely positive given that it has sharpened consumer focus on hygiene and preventative foods.

FOD’s portfolio of foods and beverages come under the banner of ‘’healthy living lifestyle’’ products, and their alignment with the sustained ‘work from home’ trend should be a demand driver.

Consumers are also increasingly shifting to "on the go" convenience foods and beverages, and FOD has a strong product offering in the sector. Today, FOD is represented in 2500 stores nationally. The plan is to be in over 5000 stores within the next 36 months.

FOD is responding to increased online consumer purchasing and this should assist in driving sales growth in 2021.

While the business was impacted last year in not being able to supply the market, the company has secured 24 month supply contracts with the major fruit growers. The prices per tonne are also commercially attractive.

Diversified brands and products targeting multiple markets

While well known for its fruit juices, FOD is starting to make its mark across the superfoods and broader health and beauty market segments within Australia, with the latter being another growth driver as the company launches new brands and products.

The recent establishment of a new state of the art wellness centre provides the capability to supply all natural wellness supplements will assist the company in accommodating increased volumes.

Not only will the new facilities provide FOD with increased production capacity, it is tailored to cater for the introduction of new products that are also backed by robust science, as well as aligning with consumer demands for healthy natural ingredients.

This has been the recipe for success for FOD’s flagship products, so rather than venturing into unknown waters, diversification should be a case of success breeding success.

Effectively, FOD will be leveraging off its brand loyalty for OBL, that is underpinned by a demonstrated track record in terms of producing healthy products.

Brand Strategy

There are three planks to FOD’s brand strategy:1. Original Juice Company (OBL)

The re- launch of the OBL Brand, now utilising only 100% Australian oranges and extending the range into cold-pressed juices, includes a 50% less sugar range and the introduction of a real fruit based range of quenchers. This has already driven the dramatic growth.

Total juice sales for the December half of fiscal 2021 were $20.7M up 15% on the previous corresponding period, (PCP) driven predominantly through the successful re-branding of Original Juice Co brand.

New products accounted for $1.5 million in additional sales, but this is an area that is expected to grow substantially in the near to medium-term.

2. Juice Lab

FOD’s new product range of Juice Lab Wellness shots is listed in Coles, Ritchies, Drakes, Foodland and Metcash.

New Original Juice Co Quenchers, with 50% less sugar and Probiotic variants, will complement the existing range, providing another avenue for growth in 2021.

FOD management also sees a significant opportunity for the Juice Lab to offer a healthy alternative in the $3 billion carbonated beverage market.

Juice Lab Carbonated Wellness Drinks are being presented to all major petrol and convenience outlets including 7- Eleven, Coles Express, Ampol, Woolworths Metro and BP.

3. Wellness supplements

In 2020, FOD developed a 1,260 square metre state-of-the-art clean room with laboratory, powder and liquid mix capabilities at Mill Park in Melbourne.

This has enabled the company to launch a range of collagen products, and the development of the wellness product range is primarily targeted to the Chinese export market. It is expected this will also boost sales and diversify FOD’s product offering.

Outside the food and beverages market segment, the group’s Eridani premium range of Marine Collagens is being rolled out on Chinese e-commerce platforms.

The collagen market is worth in excess of $4.6 billion and set to exceed $10 billion by 2025, based on it being the best source of all-natural protein.

Eridani Premium Marine Collagen focuses on targeting the whole body with the addition of Vitamin C, Calcium and Magnesium, creating an age-defying inner beauty foundation with benefits internally and externally.

An extended range of Eridani products is being developed across FOD capabilities in powder, gel and liquid formats.

Key achievements in H1 2021

There was an impressive turnaround in the company’s financial performance in the first half of the financial year, with the group generating earnings before interest, tax, depreciation and amortisation (EBITDA) of $2.2 million (compared with $200,000 in the first half of fiscal 2020).

This was predominantly achieved on the back of strong organic growth with sales up 24% to $22.2 million.

FOD raised $4.5 million to support the rollout of new products and to assist in the implementation of further operational efficiencies. The company had cash of approximately $3 million as at 31 December, 2020.

There was an increase in production throughput at the Mill Park facility, accompanied by reduced waste and lower overall labour costs, and the associated operational efficiencies should see the company generate stronger margins in the second half.

The improvements in this area are worth underlining as they have delivered $600,000 in cost savings since mid-2020.

In brief, the factory performance continued to improve with a 27% reduction in labour cost per litre of production. Throughput via converting manufacturing lines increased by over 29% and downtime improved by 18%.

Potential share price catalysts

Aside from a share price rerating that better reflects FOD’s earnings profile and its scope for growth, FOD is shaping up as a news driven story over the next 12 months, and we will now address some of the key developments to be on the lookout for.

Following the most recent capital raise, FOD now has the balance sheet strength to increase the profile of its Original Juice Co and Juice Lab products, while also delivering new product ranges to the market in coming periods, these will be key catalysts to watch.

In terms of the company’s core business, management is positioning OBL to achieve a 15% share of the Australian juice market.

With the strong acceptance of OBL’s "50% less sugar" range, as well as probiotic variants, this could be within its grasp, representing a potential share price driver.

Expansion into functional foods, nutraceuticals and wellness supplements that improve the quality of consumers’ lives can be expected.

Just as the group’s entry into South Australia, and plans to extend availability of their products from 2500 stores to over 5000 stores over the next 3 years, will deliver strong organic growth.

With the $3 billion carbonated beverage market being such a huge opportunity where even a small slice of the pie could provide substantial sales growth, any commercial developments are likely to be viewed positively, with the prospect of impacting the group’s share price.

Management’s ability to sustain and/or build on cost savings and efficiencies realised in 2020 would be viewed as a key operational outcome.

This would be particularly true, should the flow on margin improvement strengthen the bottom line beyond what can be achieved purely from revenue growth.

Expansion into the burgeoning Chinese market could also have a significant impact on sales.

As indicated below, FOD has a number of levers to pull to achieve its goal of 16% compound annual sales growth.

Investment Overview

While FOD is generating the bulk of its revenue from one well-established brand, the broader company is very much in its infancy and as such should be valued on the basis of the growth that can be achieved off a fairly modest base.

Unlike many touted potential growth stories, FOD has proven it can generate significant growth in sales and earnings with the latter benefiting from astute operational management, a good sign for a growing business.

Having established the infrastructure to cater for an uptick in production to meet increased demand, the company shouldn’t have any near-term large capital expenditure.

Given this backdrop, FOD’s financial performance in the second half of fiscal 2021 appears fairly predictable in terms of mounting a base case scenario, not taking into account the degree of sales growth that can be realised from the rollout of new products into new and established markets.

However, FOD operates in quite a niche industry, and one probably has to look to more mature companies to find a comparison.

A full list of ASX Food product companies is here.

Beyond Maggie Beer Holdings Ltd (ASX: MBH), another that stands out is BWX Ltd (ASX: BWX), a group that also targets a market that has a strong focus on health and wellness.

While BWX’s products also fall under the fast moving consumer goods (FMCG) banner with distribution through the likes of major retail outlets, the group’s products hinge around market segments such as skincare and haircare.

This is similar to where FOD is heading with the Eridani range.

BWX isn’t involved in the food and beverage distribution industry, and it is a larger and more mature business with a market capitalisation of approximately $600 million.

However, it does have the same underlying theme in terms of using all natural products that promote health and wellness.

The company has an enterprise value of about $680 million, and based on analyst Blue Ocean Equities projections for the 12 months to June 30, 2021 BWX should generate EBITDA of $34.1 million.

This implies a fiscal 2021 enterprise value/EBITDA ratio of approximately 20.

Should FOD over the next 24 months achieve full year EBITDA of $4.4 million and trade on a similar EV/EBITDA to BWX, this would imply an enterprise value of $88 million.

Based on the group’s share price of 3.3 cents on 2 March 2021, FOD has a market capitalisation of approximately $26.4 million.

Given the company had cash of about $3 million as at 31 December 2020, FOD’s enterprise value is in the vicinity of $23.4 million.

Consequently, if the company was to be valued on similar multiples as BWX it would need to be trading in the vicinity of 12 cents per share, implying a share price increase of about 265%.

While direct comparisons with the much larger BWX can’t be used to estimate a share price target, there are industry norms that provide a rough estimate.

Suffice to say though that it appears there is the potential for FOD to undergo a value-based rerating, particularly if it achieves or surpasses the aforementioned earnings levels in fiscal 2021.

THE BULLS SAY

- As indicated above, a peer comparison tends to suggest that FOD is undervalued based on financial metrics, with little recognition of the scope to grow rapidly off a relatively modest base.

- From a macro perspective, there is increasing demand for all-natural products such as those produced by FOD across the food, beverage and health and wellness sectors.

- Improved margins should be achieved through increased scale and the ongoing introduction of efficiencies in production and distribution.

- Revenue growth should be driven by increased sales of established products and the rollout of new products, as well as expansion into new markets where China could play a vital role - for example, just a small share of the $3 billion carbonated beverage market would be transformational.

- FOD has the balance sheet strength to increase the profile of its Original Juice Co and Juice Lab products, while also delivering new product ranges to the market in coming periods.

- The negotiation of commercial agreements that broaden the company’s areas of distribution, are likely to occur more frequently in 2021 given FOD’s more comprehensive product range.

- With FOD Represented in only 2 500 stores in Australia today and competitors such as Coca Cola and other beverage companies represented in over 15 000 stores, there is massive upside just getting current Brand porfolio into more points of availability.

THE BEARS SAY

- Competition in the fast moving consumer goods industry can be fierce, and supermarkets have a history of being price makers rather than price takers, as well as promoting their own brand products ahead of external suppliers.

- Launching new products can be challenging even though FOD is sticking with its unique brand signature.

- COVID remains an issue that could place downward pressure on the broader retail industry in 2021.

- Should FOD be successful in achieving substantial growth there may come a time when it requires additional plant and equipment for production - smaller companies can at times experience challenges in raising capital to meet their needs. That said, if the company maintains its earning trajectory, it should have a range of debt and equity options.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.