Cornerstone funding as demand accelerates

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Overview: Crowd Mobile Limited ("Crowd Mobile", "the Company") is an Australian technology Company focused on mobile software and services. Its principal assets include product distribution capability via 60 mobile phone carriers in 25 countries, and proprietary content production capabilities focused on consumer advice. Founded in 2005, the Company listed on the ASX via a reverse merger with Q Limited. After entering into a Heads of Agreement to acquire Netherlands-based Track Holdings BV ("Track"), Crowd Mobile has announced FY15 results, expanded its product portfolio, and secured a cornerstone funding facility.

Catalysts: Execution of the Track acquisition is approaching and Crowd Mobile is witnessing strong organic growth. FY15 revenues increased 31 percent whilst utilisation of its ‘message’ services is accelerating. Volumes have increased for five consecutive quarters and last month’s launch of the ‘Crowd Butler’ transaction service represents the first in a series of next-generation consumer products designed to leverage its distribution assets. The Track driven expansion of Crowd Mobile’s distribution base is now supported by a debt offer representing 40 percent of the deal value. Discussions regarding the balance are advanced.

Hurdles: With the quantum of service deliveries across its network increasing at double the pace of FY15 revenue, there is a risk that recent growth is coming at the expense of margin contraction. The pending Track acquisition remains subject to funding and integration risks. With entry barriers to the industry primarily limited to complexities surrounding the procurement of carrier relationships, Crowd Mobile may face increasing competition.

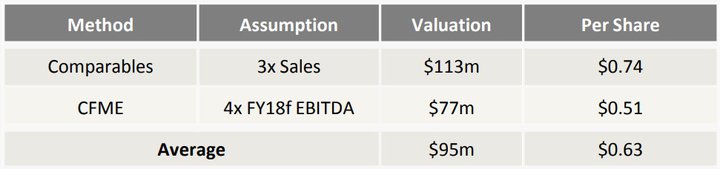

Investment View: Crowd Mobile provides profitable exposure to the market for mobile software and services. We remain attracted to the Company’s income profile and growth potential. With Crowd Mobile’s FY15 results and ‘Crowd Butler’ launch demonstrating the sound capacity to leverage existing distribution assets, finalisation of Track acquisition funding is the major near-term driver. Recent debt initiatives support our existing valuation of $0.63/share. Representing a premium of ~100 percent to recent trade, we maintain our ‘buy’ recommendation.

THE BULLS AND THE BEARS

THE BULLS SAY

- Crowd Mobile’s capacity to leverage existing distribution assets appears sound, with service volumes rising for five consecutive quarters, FY15 revenue increasing over 30 percent, and the Company launching a new generation of services via ‘Crowd Butler’

- The pending Track deal significantly enhances Crowd Mobile’s distribution capability expanding the quantity of mobile carrier relationships by 170 percent and national markets by 100 percent

- Funding risks associated with the Track acquisition are being mitigated, with Crowd Mobile procuring a debt facility representing 40 percent of the transaction value

- The Track debt facility supports our existing $0.63/share valuation, which represents a significant premium to recent trade

THE BEARS SAY

- With service volumes rising substantially faster than revenues in FY15, there is a risk that less profitable growth is being pursued

- Track is a large acquisition relative to the size of Crowd Mobile’s existing operations and there is no guarantee synergies targeted will materialise

- There is no guarantee the Track acquisition will proceed with more than half of the required funding yet to be secured

- Valuation is contingent on Crowd Mobile delivering a sustained period of earnings growth and successfully financing the Track acquisition utilising debt and hybrid securities.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.