Emerging Companies: Grange Resources Ltd (ASX: GRR)

Published 21-MAR-2014 00:00 A.M.

|

2 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

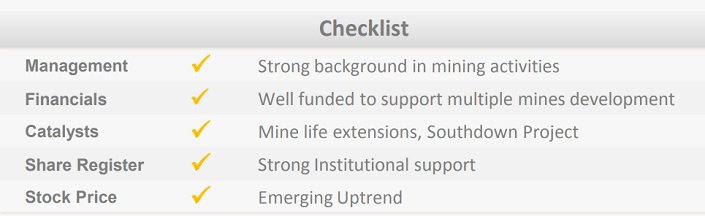

Overview: Grange Resources Limited ("Grange", the Group") is the largest integrated iron ore pellet producer in Australia. It owns and operates the Savage River magnetite iron ore mine in north-west Tasmania and the associated pellet plant and port facility on the State’s north-west coast. The initial capex for Grange’s 70:30 JV project, Southdown Magnetite, estimated at $2.89b with its operating costs estimated at $58.5/T (April’12). During FY13, the Company completed the relocation of its corporate headquarters from Perth to Tasmania.

Catalysts: Grange posted the highest ever iron ore quarterly production of 0.62MT in 4Q13 (4Q12:0.44MT) followed by management guidance of 2.3MT in FY14. Retrieving access to North pit premium-grade ore in 3Q13 led to improved average price realizations of US$149.4/T in 4Q13 (4Q12: US$123.84/T). The advanced phase Southdown Project can add up to 6.6MT p.a., and induction of an equity partner is expected to drive growth. The recently announced 107MT resources at Long Plains and focus on mining development at multiple locations indicate cumulative resources of ~340MT securing Savage River mine life extension to 2030 and beyond.

Hurdles: Future cash flows remain subject to unfavorable exchange rate movements and commodities price fluctuations. The slowdown in demand from Asian regions or failure to secure new fixed long-term contracts may result in inventory pile–up.

Investment View: The trend for iron-ore and pellet premiums is likely to continue in FY14 due to an upsurge in demand for high-grade ore on the back of Chinese government regulatory compulsions. We are attracted to management’s rich background in the mining industry, Grange’s strong funding positions, and positive operating cash flow profile. Its strategic position as the supplier of premium grade ore and commercialization of South Pit mine in 2014/15 offering strong leverage to the upcoming global demand for steel and we initiate coverage with a ‘buy’ recommendation.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.